-

Explain why the following conditions are necessary for photosynthesis

a. Carbon (IV) Oxide

b. Light

c. Chlorophyll

d. Suitable temperature and pH

e. Water

Date posted:

May 13, 2021

-

The current through a 0.1-H inductor is i(t)=10te-5tA. Find the

(a) Voltage across the inductor and

(b) The energy stored in it.

Date posted:

May 12, 2021

-

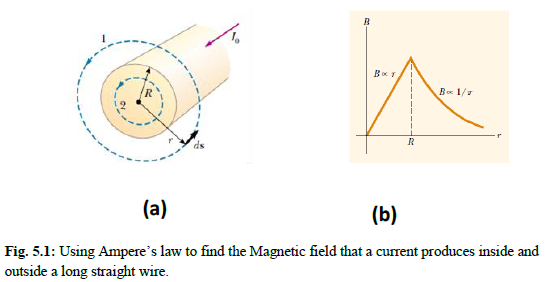

A long, straight wire of radius R carries a steady current I0 that is uniformly distributed through

the cross-section of the wire (Fig. 5.1). Using Ampere’s law, calculate the magnetic field a

distance r from the center of the wire in the regions r > R and r < R .

Date posted:

May 12, 2021

-

A wire carries a current of 22.0 A from West to East. Assume that at this location the magnetic

field of Earth is horizontal and directed from south to north and that it has a magnitude of

0.500 x 10-4 T.

(a) Find the magnitude and direction of the magnetic force on a 36.0-m length of wire.

(b) Calculate the gravitational force on the same length of wire if it’s made of copper and has a

cross-sectional area of 2.50 x 10-6 m2.

Date posted:

May 12, 2021

-

A proton moves at 8.00 x 106 m/s along the x-axis. It enters a region in which there is a magnetic

field of magnitude 2.50 T, directed at an angle of 60.0° with the x-axis and lying in the xy - plane

(Fig. 4.3). Find the initial magnitude and direction of the magnetic force on the proton.

Date posted:

May 12, 2021

-

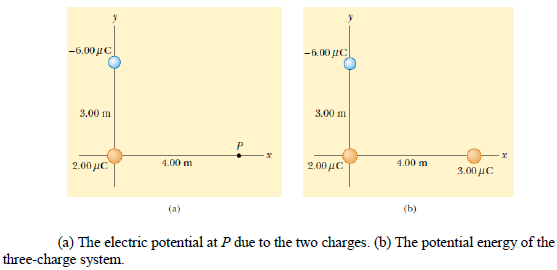

A charge q1 = 2.00 μC is located at the origin, and a charge q2 = -6.00 μC is located at (0, 3.00)

m, as shown in figure a.

(a) Find the total electric potential due to these charges at the point P, whose coordinates are

(4.00, 0) m.

(b) Find the change in potential energy of a 3.00 μC charge as it moves from infinity to point P

of (Fig a) such that the situation is as in Fig b.

(a) Find the total electric potential due to these charges at the point P, whose coordinates are

(4.00, 0) m.

(b) Find the change in potential energy of a 3.00 μC charge as it moves from infinity to point P

of (Fig a) such that the situation is as in Fig b.

Date posted:

May 11, 2021

-

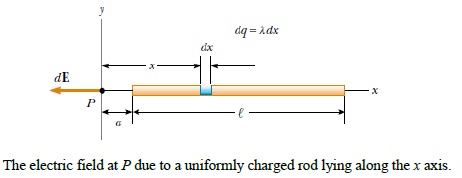

A rod of length l has a uniform positive charge per unit length λ and a total charge Q. Calculate the electric field at a point P that is located along the long axis of the rod and a distance a from one end.

Date posted:

May 11, 2021

-

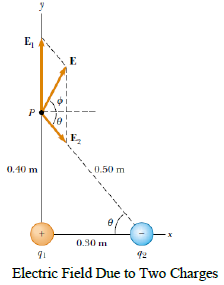

A charge q1 = 7.0 μC is located at the origin, and a second charge q2 = -5.0μC is located on the x

axis, 0.30 m from the origin. Find the electric field at the point P, which has coordinates (0, 0.40) m.

Date posted:

May 11, 2021

-

Three point charges lie along the x axis as shown in figure 2.2. The positive charge q1 =15.0μC is

at x = 2.00 m, the positive charge q2 = 6.00 μC is at the origin, and the resultant force acting on

q3 is zero. What is the x coordinate of q3?

Date posted:

May 11, 2021

-

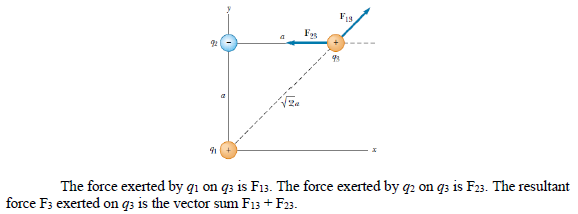

Consider three point charges located at the corners of a right triangle as shown in figure 2.1, where q1= q3 = 5.0 μC, q2 = -2.0 μC and a = 0.10 m. Find the resultant force exerted on q3.

Date posted:

May 11, 2021

-

How much charge is represented by 4,600 electrons?

Date posted:

May 11, 2021

-

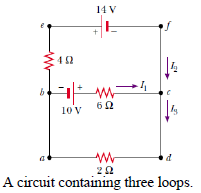

Find the currents l1, l2, and l3 in the circuit shown in figure below.

Date posted:

May 11, 2021

-

A cell of unknown emf E and internal resistance 2 Ω is connected to a 5 Ω resistance. If the terminal p.d V is 1.0 V, calculate E.

Date posted:

May 11, 2021

-

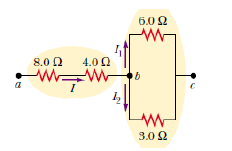

Four resistors are connected as shown in figure below.

(a) Find the equivalent resistance between points a and c.

(b) What is the current in each resistor if a potential difference of 42 V is maintained between a and c ?

(a) Find the equivalent resistance between points a and c.

(b) What is the current in each resistor if a potential difference of 42 V is maintained between a and c ?

Date posted:

May 11, 2021

-

In transportation problems the following difficulties do occur;

degeneracy, inequality of supply and demand and non - unique optimal solution.

Required:

(i) Explain the underlined words.

(ii) Explain how the transportation algorithm is adapted to overcome the above difficulties.

Date posted:

May 10, 2021

-

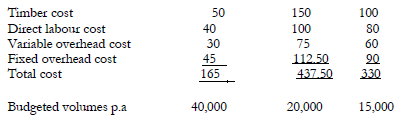

Chemex limited manufactures three garden furniture products A B and C. The budgeted unit cost and resource requirements of each of these items are detailed below.

These volumes are believed to equal the market demand for these products. The fixed

overhead costs are attributed to the three products on the basis of direct labour hours. The

labour rate is Shs 40 per hour. The cost of the timber is Shs 20 per square metre. The

products are made from a specialist timber.

A memo from the procurement manager advises you that because of a problem with the

supplier it is to be assumed that this specialist timber is limited in supply to 20,000 square

metres per annum.

The sales director has already accepted an order for 5,000 A, 1,000B and 1,500C, which if

not supplied would incur a financial penalty of Shs 20,000. These quantities are included in

the market demand estimates above.

The selling prices of the three products are:

A = Shs 200

B = Shs 500

C = Shs 400

Required

a) Determine the optimum production plan and state the net profit that this should

yield per annum.

b) Calculate and explain the maximum prices, which should be paid per square metre in

order to obtain extra supplies of the timber.

These volumes are believed to equal the market demand for these products. The fixed

overhead costs are attributed to the three products on the basis of direct labour hours. The

labour rate is Shs 40 per hour. The cost of the timber is Shs 20 per square metre. The

products are made from a specialist timber.

A memo from the procurement manager advises you that because of a problem with the

supplier it is to be assumed that this specialist timber is limited in supply to 20,000 square

metres per annum.

The sales director has already accepted an order for 5,000 A, 1,000B and 1,500C, which if

not supplied would incur a financial penalty of Shs 20,000. These quantities are included in

the market demand estimates above.

The selling prices of the three products are:

A = Shs 200

B = Shs 500

C = Shs 400

Required

a) Determine the optimum production plan and state the net profit that this should

yield per annum.

b) Calculate and explain the maximum prices, which should be paid per square metre in

order to obtain extra supplies of the timber.

Date posted:

May 10, 2021

-

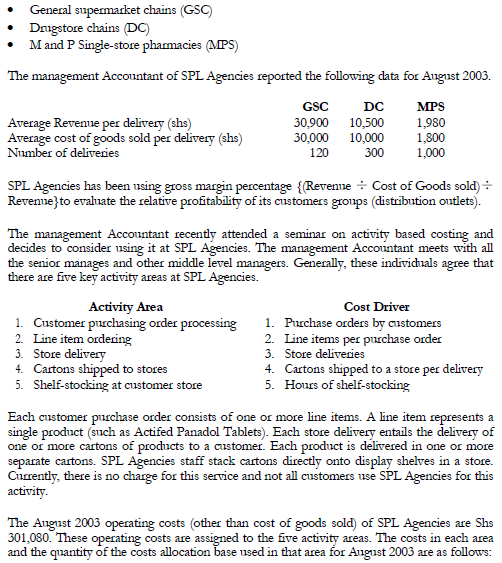

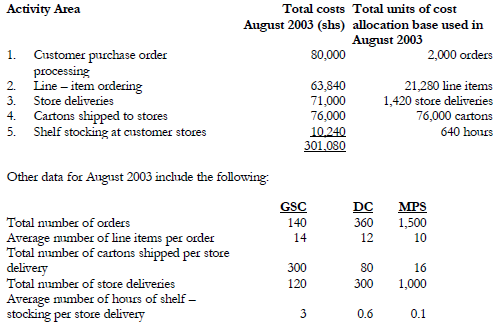

SPL Agencies specializes in the distribution of pharmaceutical products. They buy from pharmaceutical companies and resells to each of three different markets.

Required:

(a) Compute the August 2003 gross – margin percentage for each of its three distribution

markets and SPL Agencies operating income.

(b) Compute the August 2003 rate per unit of the cost allocation base for each of the five

activity areas.

(c) Compute the operating income of each distribution market in August 2003 using the

activity based costing information. Comment on the results.

Required:

(a) Compute the August 2003 gross – margin percentage for each of its three distribution

markets and SPL Agencies operating income.

(b) Compute the August 2003 rate per unit of the cost allocation base for each of the five

activity areas.

(c) Compute the operating income of each distribution market in August 2003 using the

activity based costing information. Comment on the results.

Date posted:

May 8, 2021

-

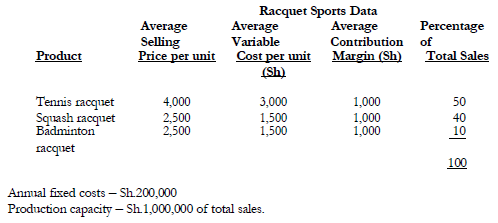

Racquet Sports produces a variety of racquets for the sports industry. It makes racquets for tennis, squash and badminton. The table below presents the relevant data for the products produced.

Required:

a) (i) Determine the contribution percentage on each shillings of sales for each of the

products produced and sold.

(ii) What is the overall contribution that each sales shillings provides toward covering

the firm‟s fixed costs, that is overall break-even point in shillings sales?

(iii) Determine the profits if the plants operates at 70 per cent of the plant capacity.

b) Explain the limitations of the techniques you have used to solve part (a) above.

Required:

a) (i) Determine the contribution percentage on each shillings of sales for each of the

products produced and sold.

(ii) What is the overall contribution that each sales shillings provides toward covering

the firm‟s fixed costs, that is overall break-even point in shillings sales?

(iii) Determine the profits if the plants operates at 70 per cent of the plant capacity.

b) Explain the limitations of the techniques you have used to solve part (a) above.

Date posted:

May 8, 2021

-

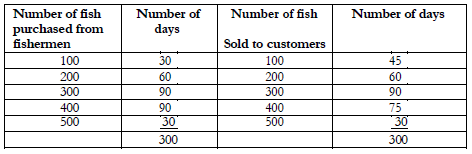

Peter Oloo is a fishmonger in Kisumu. As a result of adverse business changes in the region,

the supply and demand for fish are subject to random variations making it difficult to

project the next day‟s business.

Management accounts in relation to the previous 300 days reveal the following mode of behaviour:

Peter Oloo buys each fish at Sh.40 and sells it for Sh.60 if sold on the same day; if the fish is

sold the following day it will fetch only Sh.20. If not sold during the second day its value

drops to zero and Peter Oloo do nates it to children‟s home. Peter Oloo‟s Policy is to

satisfy the days demand from the fresh fish first; and any further demand will be satisfied

from the stock of fish from previous day. Failure to satisfy demand costs Peter Oloo Sh.20

for every fish supplied to the customer. There are no back orders in the business.

Required:

a) Simulate Peter Oloo's operations for 8 days clearly indicating profits made each day.

b) What are the average daily profits for Peter Oloo?

Use the following random numbers

573423709751483681320931644925928345

Peter Oloo buys each fish at Sh.40 and sells it for Sh.60 if sold on the same day; if the fish is

sold the following day it will fetch only Sh.20. If not sold during the second day its value

drops to zero and Peter Oloo do nates it to children‟s home. Peter Oloo‟s Policy is to

satisfy the days demand from the fresh fish first; and any further demand will be satisfied

from the stock of fish from previous day. Failure to satisfy demand costs Peter Oloo Sh.20

for every fish supplied to the customer. There are no back orders in the business.

Required:

a) Simulate Peter Oloo's operations for 8 days clearly indicating profits made each day.

b) What are the average daily profits for Peter Oloo?

Use the following random numbers

573423709751483681320931644925928345

Date posted:

May 8, 2021

-

Briefly give five examples of business applications of linear programming.

Date posted:

May 8, 2021

-

Mitumba Ltd. has set the following standards:

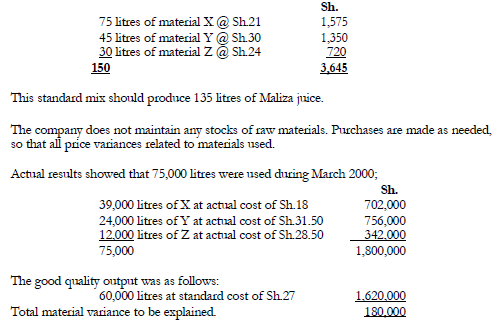

Required:

Comprehensive computation showing the yield, mix and price variances.

Required:

Comprehensive computation showing the yield, mix and price variances.

Date posted:

May 8, 2021

-

Uchunguzi Ltd. plans to conduct a questionnaire survey. The table below shows the tasks involved, the immediately proceeding tasks and for each task duration the most likely estimate (L), optimistic estimate (O) and the pessimistic estimate (P).

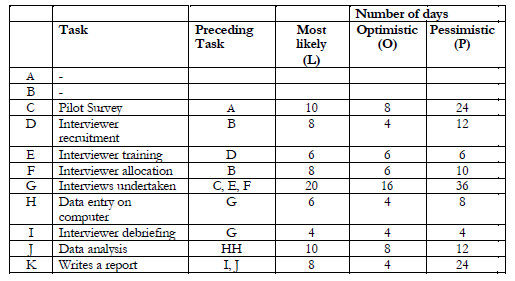

Using the project evaluation and review technique (PERT) the meantime, M and standard

deviation O. for the duration of each task are estimated from t he most likely (L), Optimistic

(O) pessimistic (P) estimates by using the formulae:

M = 0.08333 (4L + O + P)

O = 0.08333 (P – O)

Required:

a) Compute the mean duration and standard deviation for each task.

b) The project is budgeted to cost Sh.500,000. Actual costs per day are Sh.10,000.

Can the project be implemented within the budget?

Using the project evaluation and review technique (PERT) the meantime, M and standard

deviation O. for the duration of each task are estimated from t he most likely (L), Optimistic

(O) pessimistic (P) estimates by using the formulae:

M = 0.08333 (4L + O + P)

O = 0.08333 (P – O)

Required:

a) Compute the mean duration and standard deviation for each task.

b) The project is budgeted to cost Sh.500,000. Actual costs per day are Sh.10,000.

Can the project be implemented within the budget?

Date posted:

May 8, 2021

-

Kutwa Ltd. is a manufacturing company with two divisions; A and B. Division A

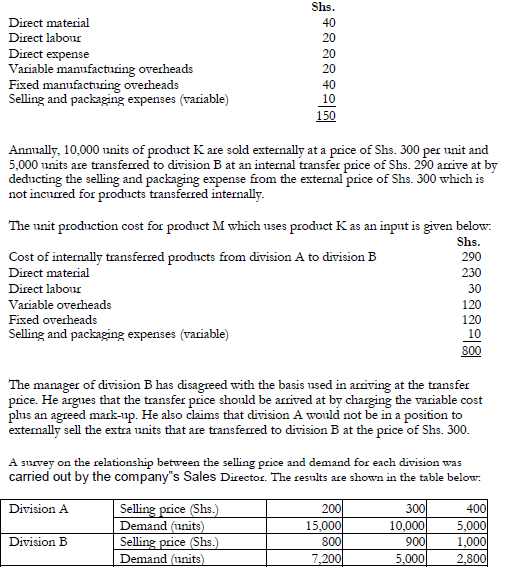

manufactures a single standard product K, some of which is sold externally and the

remainder used as an input in division B in the manufacture of product M.

The unit production costs of product K are given below:

The manager of division B suggests that based on the above results, a transfer price of Shs.

120 would offer division A a reasonable contribution towards its fixed cost and earn

division B a reasonable profit. This would lead to an increase in the output and overall

profitability of the company.

Required:

( a) Calculate the effect of the existing transfer pricing system on the company‟s profits.

( b) Calculate the effect of adopting the transfer price of Shs. 120 on the company‟s

profits.

The manager of division B suggests that based on the above results, a transfer price of Shs.

120 would offer division A a reasonable contribution towards its fixed cost and earn

division B a reasonable profit. This would lead to an increase in the output and overall

profitability of the company.

Required:

( a) Calculate the effect of the existing transfer pricing system on the company‟s profits.

( b) Calculate the effect of adopting the transfer price of Shs. 120 on the company‟s

profits.

Date posted:

May 7, 2021

-

Transfer pricing of products between processes in a manufacturing company can be done at:

1. Cost or

2. Sales value at the point of transfer.

Required:

Discuss how each of the above methods could be used effectively in the operations

of a responsibility accounting system.

Date posted:

May 7, 2021

-

Makazi Ltd. manufactures a hedge-trimming tool which has been selling at Shs.

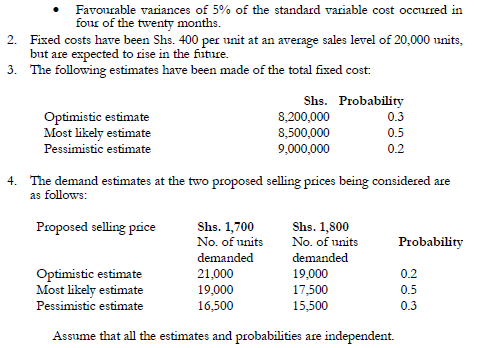

1,600 per unit for a number of years. The selling price is to be reviewed and the

following information is available on costs and the likely demand:

1. The standard variable cost of manufacturing the tool is Shs. 1,000 per unit and

an analysis of the cost variances in the past 20 months shows the following

pattern which the production manager expects to continue in the future.

Adverse variances of 10% of the standard variables cost occurred in ten

of the twenty months.

Nil variances occurred in six of the twenty months.

Required:

(i) Based on the information given above, advise the management of Makazi Ltd.

on whether they should change the selling price. Indicate the price you would

recommend.

(ii) The expected profit at the price you have recommended in (i) above and the

resulting margin of safety expressed as a percentage of expected sales

(iii) Comment on the method of analysis you have used to deal with the

probabilities given in the question.

(iv) Explain briefly how the use of a computer program would improve your

analysis.

Required:

(i) Based on the information given above, advise the management of Makazi Ltd.

on whether they should change the selling price. Indicate the price you would

recommend.

(ii) The expected profit at the price you have recommended in (i) above and the

resulting margin of safety expressed as a percentage of expected sales

(iii) Comment on the method of analysis you have used to deal with the

probabilities given in the question.

(iv) Explain briefly how the use of a computer program would improve your

analysis.

Date posted:

May 7, 2021

-

Equi -solutions Ltd. was formed ten years ago to provide business equipment solutions to

local business. It has separate divisions for research, marketing, product design, technology

and communication services, and now manufactures and supplies a wide range of business

equipment. To date the company has evaluated its performance using monthly financial

reports that analyze profitability by type of equipment. The managing director of Equi solutions

Ltd. has recently returned from a course in which it has been suggested that the

“Balanced Scorecard” could be a useful way of measuring performance.

Required:

a) Explain the “Balanced Scorecard” and how it could be used by Equi-solutions Ltd. to

measure its performance.

b) The managing director of Equi-solutions Ltd. also overheard someone mention how the

performance of their company had improved after they introduced “Bench marking.”

Required:

Explain “Bench-marking” and how it could be used to improve the performance of

Equi -solutions Ltd.

Date posted:

May 7, 2021

-

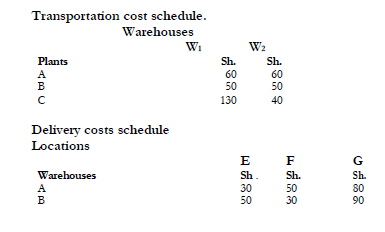

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may be distributed through any combination of the two

company warehouses W1 and W2.

2. The available monthly production capabilities for the new products are:

1000 units at plant A

2000 units at plant B

1000 units at plant C

3. Three major concentration points of customer demand are at locations E, F

and G which are estimated to have a monthly demand of:

900 units at E

800 units at F

900 units at G

4. The unit production costs amount to Sh.30, Sh.40, Sh.10 at A, B and C

respectively.

5. The unit handling costs at the warehouses amount to Sh.20 and Sh.30 at W1

and W2.

6. The unit transportation costs from plant to warehouse and unit delivery cost

from warehouse to customers are as shown below:

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Date posted:

May 7, 2021

-

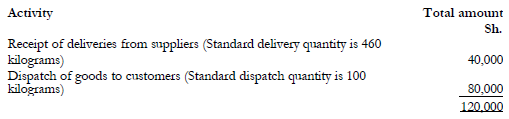

Industrial Chemical Ltd. (ICL) produces chemical Y. the standard ingredients of 1 kilogram

of Y are:

0.65 kilograms of ingredient F @ Sh. 40 per Kg

0.30 kilograms of ingredient D @ Sh. 60 per Kg.

0.20 kilograms of ingredient N @ Sh. 25 per Kg.

The following additional information is provided:

1. Production of 4,000 kilograms of chemical Y was budgeted for October 2004.

2. The production of chemical Y is entirely automated and production costs attributed to

its production comprise only direct materials and overheads.

3. ICL‟s production process works on a just-in-time (JIT) inventory system and

no ingredients or inventories of chemical Y are held.

4. Overheads budgeted for the production of Y in the month of October 2004 were as

follows:

5. In October 2004, 4,200 kilograms of Y were produced and the cost details were as

follows:

Materials used

2,840 kilograms of F, 1,210 kilograms of D and 860 kilograms of N at a total cost of

Sh. 203,800.

Actual overhead costs

12 supply deliveries at a cost of Sh.48,000 and 38 customer dispatches at a cost of

Sh. 78,000 were made.

6. ICL‟s budget committee met recently to discuss the preparation of the cost

control report for October 2004 and the following discussion took place:

Chief accountant: “the overheads do not vary directly worth output and

are therefore by definition „fixed‟. They should be analyzed and reported

accordingly”.

Management accountant: “the overheads do not vary with output, but they

are certainly not fixed. They should be analyzed and reported on an activity based

basis.”

Required:

Having regard to this discussion,

a) Prepare a variance analysis of the production costs of Y in October 2004. (Separate the

material cost variance into price, mixture and yield components and the overhead cost

variance into expenditure, capacity and efficiency components using consumption of

ingredient F as the overhead absorption base).

b) Prepare a variance analysis of the overhead production costs on Y in October 2004 on

an activity based basis.

5. In October 2004, 4,200 kilograms of Y were produced and the cost details were as

follows:

Materials used

2,840 kilograms of F, 1,210 kilograms of D and 860 kilograms of N at a total cost of

Sh. 203,800.

Actual overhead costs

12 supply deliveries at a cost of Sh.48,000 and 38 customer dispatches at a cost of

Sh. 78,000 were made.

6. ICL‟s budget committee met recently to discuss the preparation of the cost

control report for October 2004 and the following discussion took place:

Chief accountant: “the overheads do not vary directly worth output and

are therefore by definition „fixed‟. They should be analyzed and reported

accordingly”.

Management accountant: “the overheads do not vary with output, but they

are certainly not fixed. They should be analyzed and reported on an activity based

basis.”

Required:

Having regard to this discussion,

a) Prepare a variance analysis of the production costs of Y in October 2004. (Separate the

material cost variance into price, mixture and yield components and the overhead cost

variance into expenditure, capacity and efficiency components using consumption of

ingredient F as the overhead absorption base).

b) Prepare a variance analysis of the overhead production costs on Y in October 2004 on

an activity based basis.

Date posted:

May 7, 2021

-

The Marima Manufacturing Company produces four products; W, X, Y and Z using

the same plant and processes.

The following information relates to the company:

Required:

(i) Unit costs per product using activity-based costing tracing costs to production units by

means of cost drivers.

(ii) Comment briefly on the differences disclosed between overheads traced by the present

system and those traced by activity based costing.

Required:

(i) Unit costs per product using activity-based costing tracing costs to production units by

means of cost drivers.

(ii) Comment briefly on the differences disclosed between overheads traced by the present

system and those traced by activity based costing.

Date posted:

May 6, 2021

-

State the factors to be taken into consideration when establishing the length of a budget period.

Date posted:

May 6, 2021