-

Explain the factors that are considered in the design of an organization structure.

Date posted:

April 29, 2021

-

“Outsourcing some of an organization’s operations could lead to increased productivity.” Discuss.

Date posted:

April 29, 2021

-

Explain the importance of public relations to an organization.

Date posted:

April 29, 2021

-

Explain the three levels of strategy and the characteristics of strategic management decisions at each level.

Date posted:

April 29, 2021

-

Discuss the barriers to effective decision making in an organization and suggest ways in which management can overcome such barriers.

Date posted:

April 29, 2021

-

What are the characteristics of a good mission statement?

Date posted:

April 29, 2021

-

Discuss the contributions of scientific school of management to the study of work and its relevance to the management of organizations today.

Date posted:

April 29, 2021

-

Show how delegation of authority in an organization is influenced by the following factors:

a)Chain of command

b)Unity of command

c)Span of control

d)Line and staff relationship

Date posted:

April 29, 2021

-

Differentiate between consumer markets and industrial markets

Date posted:

April 28, 2021

-

Identify five environmental factors that affect business and explain the way in which each factor influences the marketing mix of an organization.

Date posted:

April 28, 2021

-

What factors may limit the effectiveness of a performance appraisal system

Date posted:

April 28, 2021

-

Explain the external and internal forces that may trigger change in an organization.

Date posted:

April 28, 2021

-

What factors are considered when selecting a method of forecasting?

Date posted:

April 28, 2021

-

To what extent are Henri Fayol’s principles of management relevant to the management of organizations today?

Date posted:

April 28, 2021

-

The principal of Management by Objectives was first coined by Peter F. Druker in the 1950’s. Describe the principle and its merits and demerits in the organizations.

Date posted:

April 26, 2021

-

For successful management, managers must come up with objectives before commencing operations. Explain what is meant by the term ‘objectives’ and describe the characteristics that good objectives should have.

Date posted:

April 26, 2021

-

PQR Ltd. operates a chain of supermarkets. Its strategy has been to adjust product prices to accommodate differences in customers, products, locations and other variables. The market has become increasingly competitive and PQR Ltd. has decided to change its strategy. In future, it will provide a high quality service by introducing Total Quality Management (TQM) techniques in every supermarket.

Explain the relevance of a programme of TQM for PQR Ltd. in the implementation of its new strategy.

Date posted:

April 24, 2021

-

“Some management experts feel that control (that is, setting standards, measuring performance against them and taking corrective action when needed) hinders creativity. Others take the opposite view”.

With the help of examples give arguments in support of each view.

Date posted:

April 24, 2021

-

With reference to the measurement of portfolio risk, distinguish between Portfolio theory and the Capital Asset Pricing Model (CAPM).

Date posted:

April 23, 2021

-

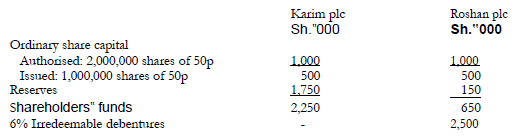

Karim plc and Roshan plc are quoted companies. The following figures are from their current balance sheets:

Both companies earn an annual profit, before charging debenture interest of Sh.500,000 which is expected to

remain constant for the indefinite future. The profits of both companies, before charging debenture interest,

are generally regarded as being subject to identical levels of risk. It is the policy of both companies to

distribute all available profits as dividends at the end of each year.

The current market value of Karim Ltd.‟s ordinary shares is Sh.3.00 per share cum div. An

annual dividend is due to be paid in the very near future.

Roshan Ltd. has just made annual dividend and interest payments both on its ordinary shares and on its

debentures. The current market value of the ordinary shares is Sh.1.40 per share and of the debentures,

Sh.50.00 percent.

Mr. Hashim owns 50,000 ordinary shares in Roshan Ltd. He is wondering whether he could increase his

annual income, without incurring any extra risk, by selling his shares in Roshan Ltd and buying some of the

ordinary shares of Karim Ltd. Mr. Hashim is able to borrow money at an annual compound rate of interest

of 12%.

You are required:

(a) to estimate the cost of ordinary share capital and the weighted average cost of capital of Karim Ltd

and Roshan Ltd;

(b) to explain briefly why both the cost of ordinary share capital and weighted average cost of capital of

Karim Ltd differ from those of Roshan Ltd;

(d) to prepare calculations to demonstrate to Mr. Hashim how he might improve his position in the way

he has suggested, stating clearly any reservations you have about the scheme; and

(d) to discuss the implications of your answers to (a), (b) and (c) above for the determination of a

company‟s optimal financial structure in practice.

Both companies earn an annual profit, before charging debenture interest of Sh.500,000 which is expected to

remain constant for the indefinite future. The profits of both companies, before charging debenture interest,

are generally regarded as being subject to identical levels of risk. It is the policy of both companies to

distribute all available profits as dividends at the end of each year.

The current market value of Karim Ltd.‟s ordinary shares is Sh.3.00 per share cum div. An

annual dividend is due to be paid in the very near future.

Roshan Ltd. has just made annual dividend and interest payments both on its ordinary shares and on its

debentures. The current market value of the ordinary shares is Sh.1.40 per share and of the debentures,

Sh.50.00 percent.

Mr. Hashim owns 50,000 ordinary shares in Roshan Ltd. He is wondering whether he could increase his

annual income, without incurring any extra risk, by selling his shares in Roshan Ltd and buying some of the

ordinary shares of Karim Ltd. Mr. Hashim is able to borrow money at an annual compound rate of interest

of 12%.

You are required:

(a) to estimate the cost of ordinary share capital and the weighted average cost of capital of Karim Ltd

and Roshan Ltd;

(b) to explain briefly why both the cost of ordinary share capital and weighted average cost of capital of

Karim Ltd differ from those of Roshan Ltd;

(d) to prepare calculations to demonstrate to Mr. Hashim how he might improve his position in the way

he has suggested, stating clearly any reservations you have about the scheme; and

(d) to discuss the implications of your answers to (a), (b) and (c) above for the determination of a

company‟s optimal financial structure in practice.

Date posted:

April 23, 2021

-

The following data have been developed for the Ujasiri Company Limited:

The yield to maturity on Treasury Bills is 0.066 and is expected to remain at this point for the

foreseeable future.

Required:

(a) The equation of the Security Market Line.

(b) The required return for the Ujasiri Company Limited.

(c) Is the Company correctly priced, underpriced or overpriced in the market? Explain.

The yield to maturity on Treasury Bills is 0.066 and is expected to remain at this point for the

foreseeable future.

Required:

(a) The equation of the Security Market Line.

(b) The required return for the Ujasiri Company Limited.

(c) Is the Company correctly priced, underpriced or overpriced in the market? Explain.

Date posted:

April 23, 2021

-

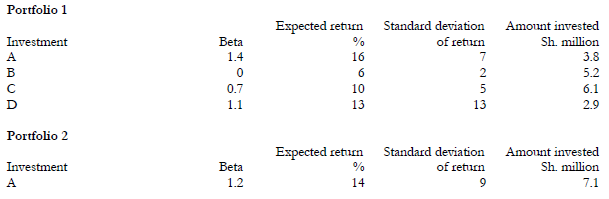

Rodfin plc is considering investing in one of two short-term portfolios of four short-term financial

investments in diverse industries. The correlation between the returns of the individual components of these

investments is believed to be negligible.

The managers of Rodfin are not sure of how to estimate the risk of these portfolios, as it has been

suggested to them that either portfolio theory or the capital asset pricing model (CAPM) will give the same

measure of risk. The market return is estimated to be 12.5% and the risk free rate 5.5%.

Required:

(a) Discuss whether or not portfolio theory and CAPM give the same portfolio risk measure.

(b) Using the above data estimate the risk and return of the two portfolios and recommend which one

should be selected.

The managers of Rodfin are not sure of how to estimate the risk of these portfolios, as it has been

suggested to them that either portfolio theory or the capital asset pricing model (CAPM) will give the same

measure of risk. The market return is estimated to be 12.5% and the risk free rate 5.5%.

Required:

(a) Discuss whether or not portfolio theory and CAPM give the same portfolio risk measure.

(b) Using the above data estimate the risk and return of the two portfolios and recommend which one

should be selected.

Date posted:

April 23, 2021

-

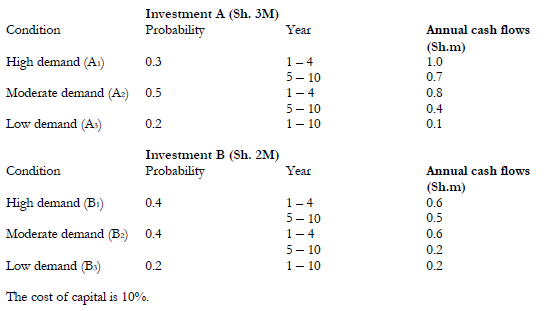

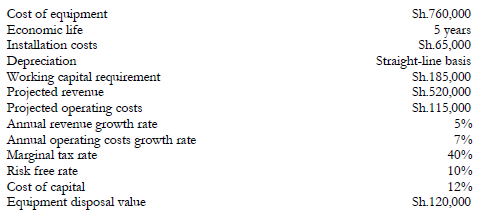

XYZ company Limited is considering a major investment in a new productive process. The total

cost of the investment has been estimated at Sh.2,000,000 but if this were increased to Sh.3,000,000,

productive capacity would be substantially increased. Because of the nature of the process, once the

basic plant has been established, to increase capacity at some future date is exceptionally costly. One

of the problem facing management is that the demand for process output is very uncertain.

However, the market research and finance departments have been able to produce the following

estimate:

Required:

Compute the expected NPV of each of the project and state the one to be chosen.

Required:

Compute the expected NPV of each of the project and state the one to be chosen.

Date posted:

April 23, 2021

-

Outline the major causes of public projects failure.

Date posted:

April 23, 2021

-

The following data have been provided with respect to three shares traded on the Nairobi

Stock Exchange (NSE).

Share A Share B Share C

Risk free rate of return 0.120 0.120 0.120

Beta coefficient 1.340 1.000 0.750

Return on the NSE index 0.185 0.185 0.185

Required:

(i) What is the beta coefficient?

(ii) Interpret the beta coefficient of shares A, B and C.

(iii) Using the Capital Asset Pricing Model, compute the expected return

on shares A, B and C.

(iv) Can the beta coefficient be less than zero? Explain

Date posted:

April 23, 2021

-

You have been provided with the following information about a project, which XYZ Ltd. is planning to undertake soon.

Required:

(a) Calculate the project‟s net investment.

(b) Using the net present value method, show whether or not the project should be undertaken by the company.

(c) Suppose in addition to the information given above you are provided with the following cash

flows certainty equivalents:

Year 0: 1.00

Year 1: 0.90

Year 2: 0.80

Year 3: 0.60

Year 4: 0.50

Year 5: 0.40

Does your conclusion about the acceptability of the project in part (c) above change? Explain.

Required:

(a) Calculate the project‟s net investment.

(b) Using the net present value method, show whether or not the project should be undertaken by the company.

(c) Suppose in addition to the information given above you are provided with the following cash

flows certainty equivalents:

Year 0: 1.00

Year 1: 0.90

Year 2: 0.80

Year 3: 0.60

Year 4: 0.50

Year 5: 0.40

Does your conclusion about the acceptability of the project in part (c) above change? Explain.

Date posted:

April 22, 2021

-

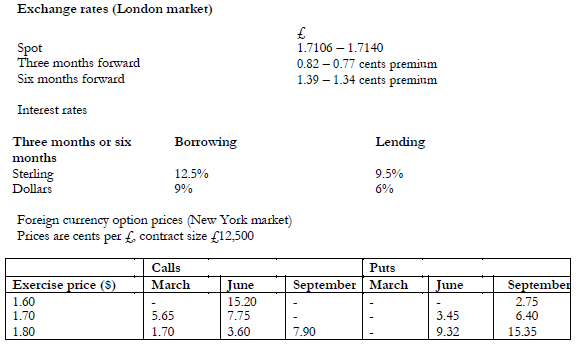

Explain briefly what is meant by foreign currency options and give examples of the advantages and disadvantages of exchange traded foreign currency options to the financial manager.

Date posted:

April 22, 2021

-

You are required to discuss whether a multinational company should hedge translation exposure by incurring transaction exposure.

Date posted:

April 22, 2021

-

A company operating in a country having the dollar as its unit of currency has today invoiced sales to the

United Kingdom in sterling, payment being due three months from the date of invoice. The invoice

amount is £3,000,000 which, at today's spot rate of 1.5985 is equivalent to USD4,795,500.

It is expected that the exchange rate will decline by about 5% over the three month period and in

order to protect the dollar proceeds from the sale, the company proposes taking appropriate

action through either the foreign exchange market or the money market.

The USD/£ three-months forward exchange rate is quoted as 1.5858-1.5873. the three-months

borrowing rate for Eurosterling is 15.0% and the deposit rate quoted by the company's own

bankers is currently 9.5%.

You are required to

Explain the alternative courses of action available to the company, with relevant calculations to four

decimal places, and to advise which course of action should be adopted.

Date posted:

April 22, 2021

-

Fidden is a medium-sized UK company with export and import trade with the USA. The following transactions are due with the next six months. Transactions are in the currency specified.

Purchases of components, cash payment due in three months: £116,000

Sales of finished goods, cash receipt due in three months: USD 197,000

Purchase of finished goods for resale, cash payment due in six months: USD 447,000

Sale of finished goods, cash receipt due in six months: USD 154,000

Assume that it is now December with three months to expiry of the March contract and that the option

price is not payable until the end of the option period, or when the option is exercised.

You are required:

(i) to calculate the net sterling receipts/payments that Fidden might expect for both its three and

six month transactions if the company hedges foreign exchange risk on:

the forward foreign exchange market; the money market.

(ii) If the actual spot rate in six months time was with hindsight exactly the present six months forward

rate, calculate whether Fidden would have been better to hedge through foreign currency

options rather than the forward market or money market.

(iii) to explain briefly what you consider to be the main advantage of foreign currency options.

Assume that it is now December with three months to expiry of the March contract and that the option

price is not payable until the end of the option period, or when the option is exercised.

You are required:

(i) to calculate the net sterling receipts/payments that Fidden might expect for both its three and

six month transactions if the company hedges foreign exchange risk on:

the forward foreign exchange market; the money market.

(ii) If the actual spot rate in six months time was with hindsight exactly the present six months forward

rate, calculate whether Fidden would have been better to hedge through foreign currency

options rather than the forward market or money market.

(iii) to explain briefly what you consider to be the main advantage of foreign currency options.

Date posted:

April 22, 2021