-

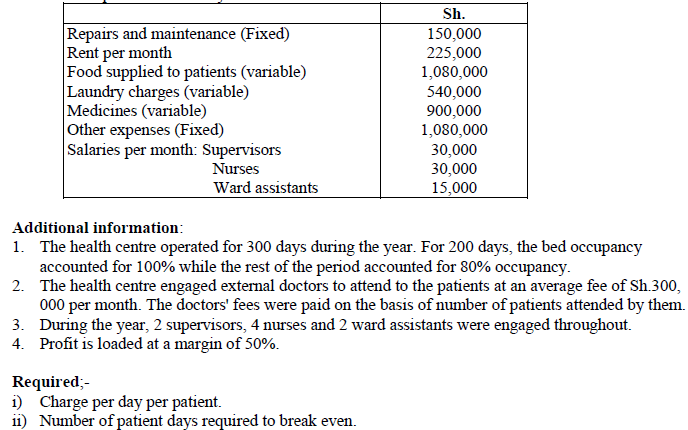

Afya Bora Health Centre has a capacity of 20 beds. The following information relates to the

centre's operations for the year ended 30 June 2014:

Date posted:

February 15, 2019

-

Highlight five circumstances under which customs duty paid might be refunded

Date posted:

February 15, 2019

-

Outline six contents of a notice of assessment.

Date posted:

February 15, 2019

-

Beta Supermarket Ltd. is registered for VAT. During the month of January 2013, the supermarket had the following transactions

January

1 Sold goods on credit to Mwamba Enterprises for Sh. 400,000.

2 Purchased goods on credit from Hekima Traders for Sh. 200,000

2 Paid for catering expenses Sh. 68,000 by cash

3 Mwamba Enterprises returned goods valued at Sh.60, 000, and received a credit note.

4 Exported goods to Uzalendo Ltd., a company based in Rwanda for Sh. 300,000

5 Purchased stationery for Sh. 84,000 on credit from Smart Books Bookshop.

9 Purchased goods for Shs 800,000 from Uchumi Enterprises on credit

12 Imported goods from Canada for Sh. 900,000 exclusive of import duty of 25% and value added tax at 16%.

16 Received a debit note of Sh. 48,000 from Uchumi Enterprises

17 Paid electricity bills amounting to Sh. 24,000 by cheque

20 Engaged an auditor and paid him Sh. 60,000 for auditing the supermarket‘s inventory.

21 Sold goods worth Sh. l,400,000 to the Ministry of Youth and Sports

24 Bought spare .parts for repair of motor vehicles for Sh. 120,000

25 Sold goods on credit to Jawabu Enterprises for Sh. 800,000

30 Made cash sales of Sh. 200,000 and banked the cash on the same day

The above transactions are stated inclusive of VAT at the rate of 16% where applicable and unless otherwise stated

Determine A value added tax (VAT) account for the month of January 2013

Date posted:

February 15, 2019

-

Daniel Mutiso, the Cost Accountant of Abra Ltd. feels that he is getting overworked and has

recommended that a management accountant be employed to take up other responsibilities in the

organization.

However, the management of the company equally argues that the work is the same and that a

decision to hire a management accountant is against their cost reduction policy.

Required:

In the light of the above statement, explain to the management three differences between management

accounting and cost accounting to help them make a fair decision.

Date posted:

February 15, 2019

-

Outline four offences under the value added tax (VAT) Act

Date posted:

February 15, 2019

-

Describe five ways in which cost accounting complements financial accounting in terms of

providing information to managers for better decision making.

Date posted:

February 15, 2019

-

Describe four shortcomings of cost accounting.

Date posted:

February 15, 2019

-

The VAT Act requires a registered person to notify the commissioner' within 14 days of changes in certain particulars of a business.

Suggest six such changes whose details need to be notified to the commissioner

Date posted:

February 15, 2019

-

Explain what 'integrated reporting' entails.

Date posted:

February 15, 2019

-

Evaluate four measures under Customs and Excise Act that are designed to prevent dumping in your country

Date posted:

February 15, 2019

-

Explain the benefits that would accrue from the adoption of international public sector accounting standards (IPSASs) by governments and public entities.

Date posted:

February 15, 2019

-

The following information has been compiled by the Ministry of Finance for the fiscal year ended 30 June 2009:

Date posted:

February 15, 2019

-

The International Public Sector Accounting Standards (IPSASs) are developed by the International Public Sector Accounting Standards Board (IPSASB) to enhance uniformity in the way public sector organizations prepare their financial statements. The Board (IPSASB) is promoting the international adoption and application of these standards.

Required:

Highlight four challenges that the Board is facing in promoting the use of IPSASs.

Date posted:

February 15, 2019

-

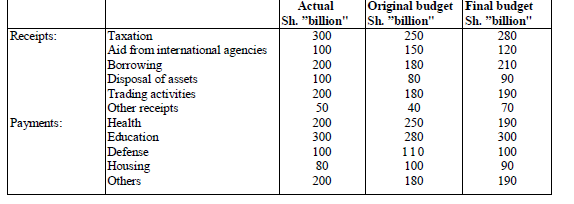

The following data has been collected from the Ministry of Trade and Commerce for the fiscal year ended 30 June 2010:

Required:

The following statements in accordance with IPSAS 1 (Presentation of Financial Statements):

i) Statement of financial performance for the year ended 30 June 2010.

ii) Statement of financial position as at 30 June 2010.

Required:

The following statements in accordance with IPSAS 1 (Presentation of Financial Statements):

i) Statement of financial performance for the year ended 30 June 2010.

ii) Statement of financial position as at 30 June 2010.

Date posted:

February 15, 2019

-

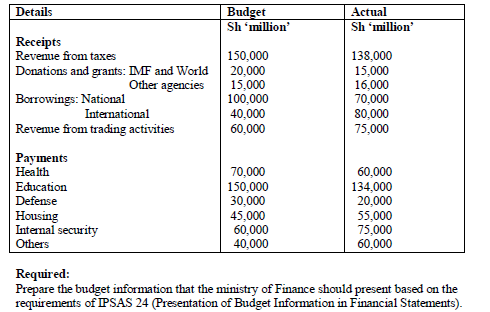

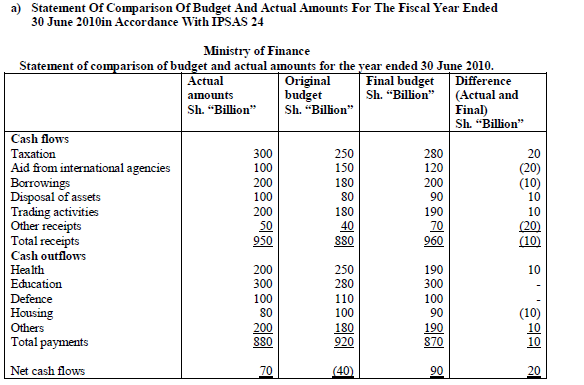

The following summary of receipts and payments was extracted from the records of the Ministry of Finance for the fiscal year ended 30 June 2010.

Required:

The statement of comparison of budget and actual amounts for the fiscal year ended 30 June 2010 in accordance with International Public Sector Accounting Standard (IPSAS) 24 (Presentation of Budget Information in Financial Statements

Required:

The statement of comparison of budget and actual amounts for the fiscal year ended 30 June 2010 in accordance with International Public Sector Accounting Standard (IPSAS) 24 (Presentation of Budget Information in Financial Statements

Date posted:

February 15, 2019

-

In the context of IPSAS 19 (Provisions, Contingent Liabilities and Contingent Assets), explain the meaning of the term 'constructive obligation'.

Date posted:

February 15, 2019

-

In the context of IPSAS 23 (Revenue from Non-exchange Transactions), summarize five sources of revenue from non-exchange transactions recognized by this standard.

Date posted:

February 15, 2019

-

Explain three benefits that could be derived from changing zero rated supplies to exempt supplies in your country

Date posted:

February 15, 2019

-

Outline four ways through which a government could prevent loss of revenue from imports

Date posted:

February 15, 2019

-

The revenue authority of your country has recently launched an online based integrated tax management system whose aim is to make it more convenient for firms and individuals to pay tax.

In light of this statement:

(i) Briefly explain how an online based integrated tax management system works.

(ii) List three types of tax returns that are filed under the system.

(iii) Evaluate five benefits that are derived from use of the system over the traditional model of filing tax returns

Date posted:

February 15, 2019

-

With reference to IPSAS 9 (Revenue from Exchange Transactions), summarize five conditions that must be satisfied before revenue from the sale of goods can be recognized.

Date posted:

February 15, 2019

-

In the context of IPSAS 4 (The Effects of Changes in Foreign Exchange Rates), explain how exchange differences arising on monetary items are recognized.

Date posted:

February 15, 2019

-

With reference to IPSAS 26 (Impairment of Non-Cash Generating Assets):

i) Explain the meaning of ‘cash-generating assets’.

ii) Analyse the criteria that could be used to identify ah asset that might be impaired.

Date posted:

February 15, 2019

-

Highlight four circumstances under which the government might revoke the licence of a manufacturer of excisable goods.

Date posted:

February 15, 2019

-

Argue four cases in favor of introduction of capital gains tax (CGT) in most countries

Date posted:

February 15, 2019

-

Outline four requirements for a valid memorandum of appeal

Date posted:

February 15, 2019

-

Summarize four details that are required to accompany the list submitted to the revenue authority on employees who have received lump sum payment from the employer.

Date posted:

February 15, 2019

-

Explain the following terms in the 'context of customs and excise duty:

(i) Prohibited goods.

(ii) Restricted goods

Date posted:

February 15, 2019

-

Benefits that a firm may enjoy by preparing a business plan.

Date posted:

February 14, 2019