-

Objectives that may be attained by establishing firms in different parts of the country

Date posted:

February 14, 2019

-

Accounting documents that are used in home trade

Date posted:

February 14, 2019

-

Disadvantages that a developing country may suffer by liberalizing foreign trade

Date posted:

February 14, 2019

-

Sources of finance for a public limited company apart from the sale of shares include:

Date posted:

February 14, 2019

-

Factors that may have caused a decline in the demand for Wooden furniture

Date posted:

February 14, 2019

-

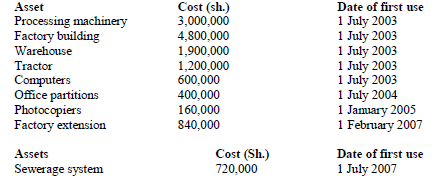

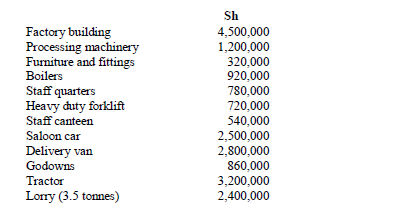

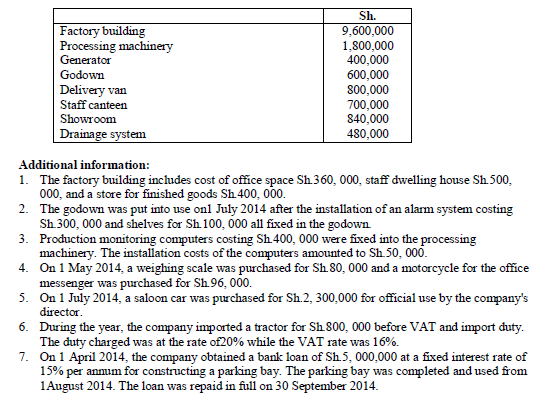

Ujenzi Limited maintained the following assets in its fixed registers as at 31 December 2007

Determine Capital allowances due to Ujenzi limited for the year ended 31 December 2007

Determine Capital allowances due to Ujenzi limited for the year ended 31 December 2007

Date posted:

February 14, 2019

-

Discuss the management of a dairy calf from birth to weaning using artificial rearing method.

Date posted:

February 14, 2019

-

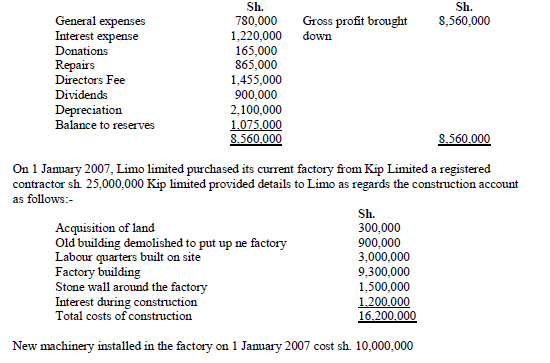

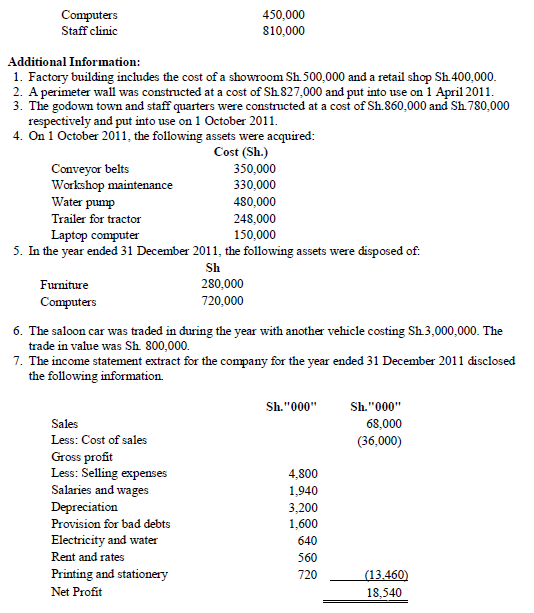

Limo Limited prepares its accounts to 31 December each year. The company‘s trading profit and loss account for the year ended 31 December 2007 is presented below

Determine:

i) Capital allowances due to Limo Limited for the year ended 31 December 2007

ii) Taxable profit (or loss) of Limo Limited for the year ended 31 December 2007

iii) Tax liability (if any) from the profit (or loss) computed in (ii) above

Determine:

i) Capital allowances due to Limo Limited for the year ended 31 December 2007

ii) Taxable profit (or loss) of Limo Limited for the year ended 31 December 2007

iii) Tax liability (if any) from the profit (or loss) computed in (ii) above

Date posted:

February 14, 2019

-

In the context of unethical management practices, discuss four incentives that could motivate the management of a business entity to manipulate the entity's financial statements as well as the underlying supporting records.

Date posted:

February 14, 2019

-

Citing two reasons, argue the case against capital allowances in an economy

Date posted:

February 14, 2019

-

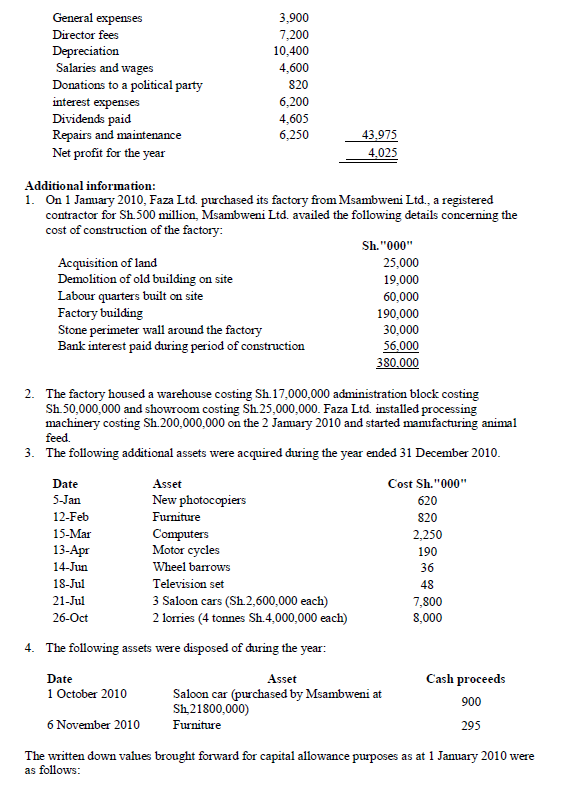

Faza Ltd. a large scale manufacturing company, has provided you with the following information for the year ended 31December 2010

Compute for Faza Ltd. for the year ended 31 December 2010:

(i) Capital allowances.

(ii) Taxable profit

Compute for Faza Ltd. for the year ended 31 December 2010:

(i) Capital allowances.

(ii) Taxable profit

Date posted:

February 14, 2019

-

Heshima Ltd. commenced operations on 1 January 2011 after incurring the following expenditure

Compute for Heshima Ltd. for the year ended 31 ended 2011

i) Capital allowances

ii) Adjusted taxable profit

Compute for Heshima Ltd. for the year ended 31 ended 2011

i) Capital allowances

ii) Adjusted taxable profit

Date posted:

February 14, 2019

-

Turbo Mining Company Ltd started prospecting for minerals in Turkana in year 2008. Expenditure relating to research, testing and winning access to minerals amounted to Sh.48 million.

The company paid Sh. 124 million to the government to acquire the rights over the minerals and shs.180 million for purchase of land.

The following assets were constructed or purchased during the year 2009:

1. Labour quarters were constructed at a cost of Sh. 15 million.

2. Senior manager's house was constructed on the site at a cost of Sh.6 million.

3. The director's house was acquired at a nearby trading centre at a cost of Sh.9 million.

4. Specialised processing machineries for mining were acquired at a cost of Sh.860 million.

5. Computers were purchased at a cost of Sh.0.72 million.

6. A forklift was acquired at a cost of Sh.4.5 million.

7. A saloon car for the general manager was purchased at a cost of Sh.3 million.

8. Office furniture was acquired at a cost of Sh. 1.5 million.

9. An aircraft was acquired for Sh. 144 million.

10. A store was constructed at a cost of Sh.21 million.

Determine The capital allowances due to the company for the years ended 31 December 2009, 2010 and 2011.

Date posted:

February 14, 2019

-

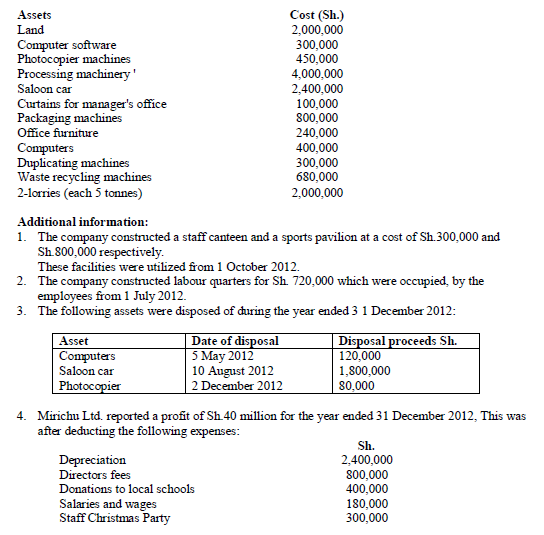

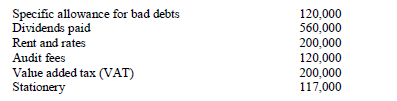

Mirichu Ltd. processes milk for sale in the local market.The company started its operations on 1 January 2012 after constructing two factory building at a cost of Sh.9 million each. Other assets acquired by the company on commencement of its operations included

Determine:

a) The capital allowances due to Mirichu Ltd. for the year ended 31 December 2012.

b) The taxable profit or loss for Mirichu Ltd. for the year ended 31 December 2012.

c) The tax- payable, if any, for the year ended 31 December 2012.

Determine:

a) The capital allowances due to Mirichu Ltd. for the year ended 31 December 2012.

b) The taxable profit or loss for Mirichu Ltd. for the year ended 31 December 2012.

c) The tax- payable, if any, for the year ended 31 December 2012.

Date posted:

February 14, 2019

-

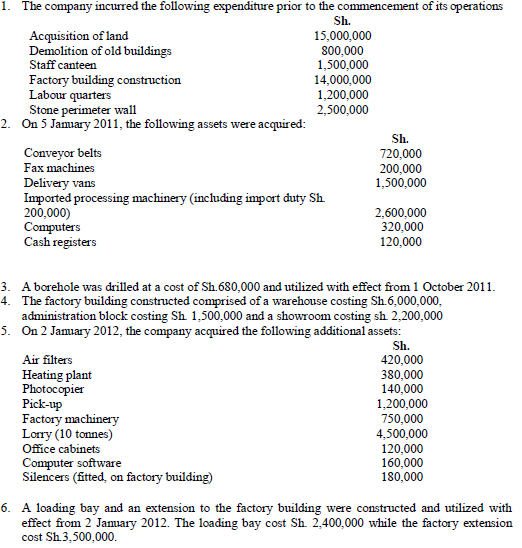

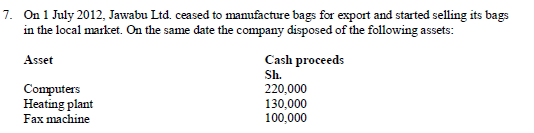

Jawabu Ltd. commenced its operations on 1 January 2011 after obtaining a licence to manufacture leather bags for export.

The following information relates to the company's operations for the financial years ended 31 December 2011 and 2012:

Determine Capital allowances due to Jawabu Ltd. for each of the two years ended 31 December 2011 and 2012.

Determine Capital allowances due to Jawabu Ltd. for each of the two years ended 31 December 2011 and 2012.

Date posted:

February 14, 2019

-

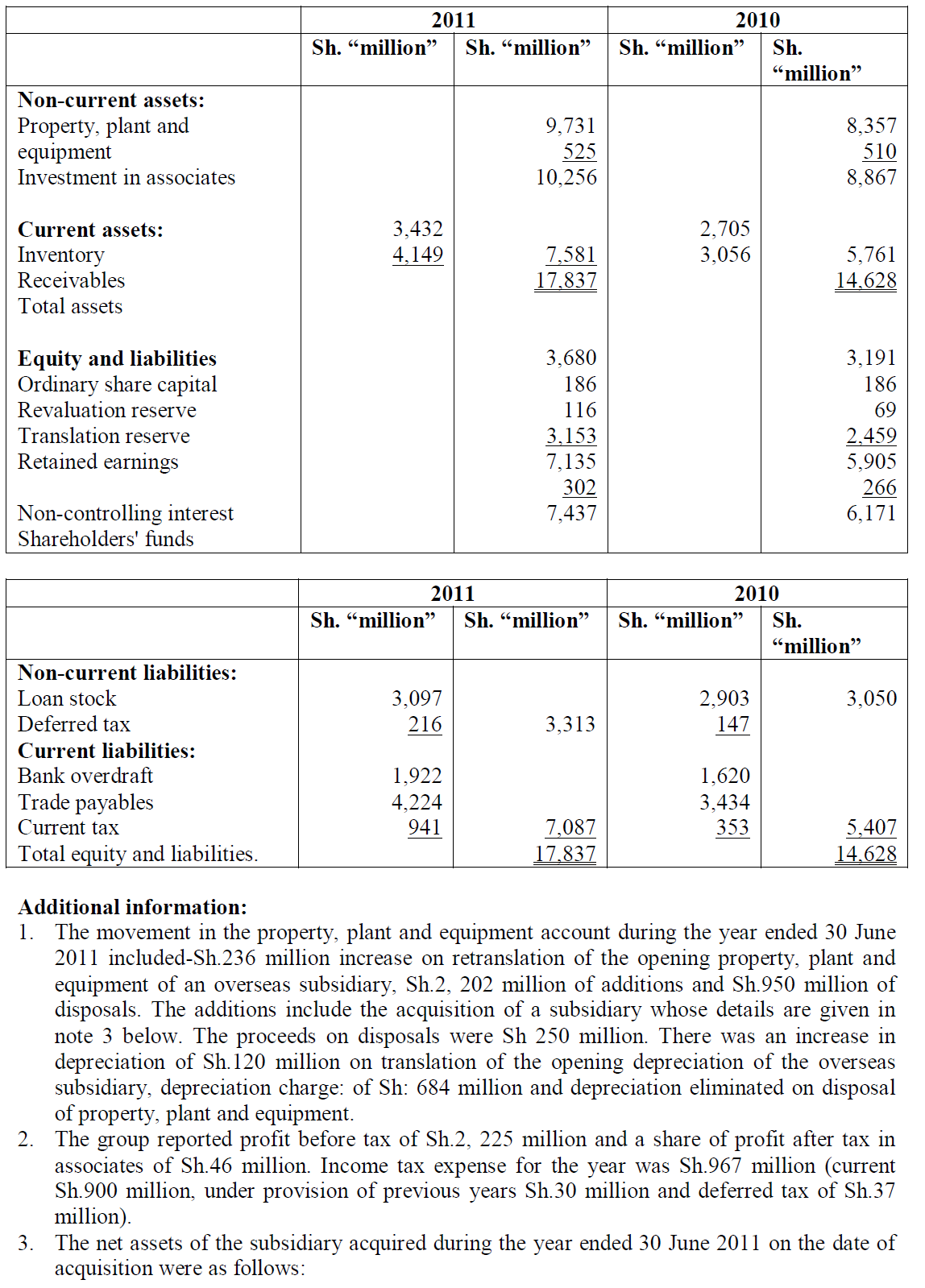

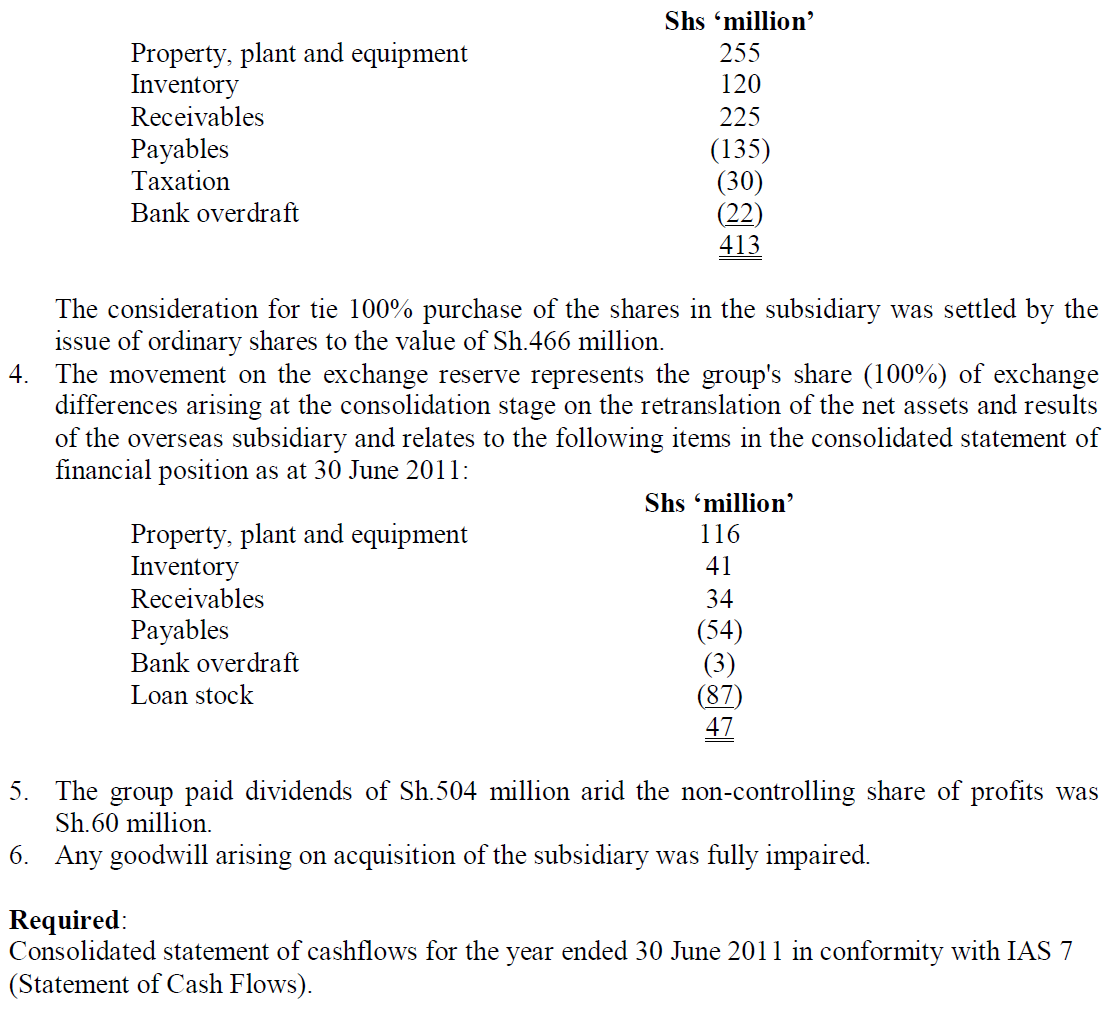

Pamoja group has-prepared the following draft statements of financial position as at 30 June:

Date posted:

February 14, 2019

-

Poland Mining Company Ltd. started prospecting for titanium in Mombasa in year 2011. Expenditure relating to research, testing and winning access to titanium amounted to Sh.240 million. The company paid Sh.720 million to the government to acquire rights over the titanium and Sh.210 million for the purchase of land.

The following assets were constructed or purchased during the year 2012:

1. Two graders were purchased at a total cost of Sh.16, 000,000.

2. A forklift was acquired at a cost of Sh.6, 000,000.

3. A store was constructed at a cost of Sh.36, 000,000

4. Office furniture was acquired at a cost of Sh.2, 400,000.

5. Labor quarters were constructed at a cost of Sh.42, 000,000.

6. Ten Lorries (5 tonnes each) were acquired at a total cost of Sh.30, 000,000.

7. Specialized processing machines for mining were acquired at a cost of Sh.960, 000,000.

8. A staff clinic was constructed at a cost of Sh.12, 000,000 .

9. Computers were purchased at a cost of Sh.480, 000.

10. A ship (600 tonnes) was acquired at a cost of Sh.450, 000,000.

11. Three saloon cars for official use were acquired at a total cost of Sh.9, 000,000.

Determine Capital allowances due to Poland Mining Company Ltd. for the two years ended 31 December 2012 and 31 December 2013

Date posted:

February 14, 2019

-

Dellite Ltd. is a manufacturing company which commenced business on 1st October 2013 after incurring the following capital expenditure

Determine Capital allowances due to Dellite Ltd. for the year ended 30 September 2014

Determine Capital allowances due to Dellite Ltd. for the year ended 30 September 2014

Date posted:

February 14, 2019

-

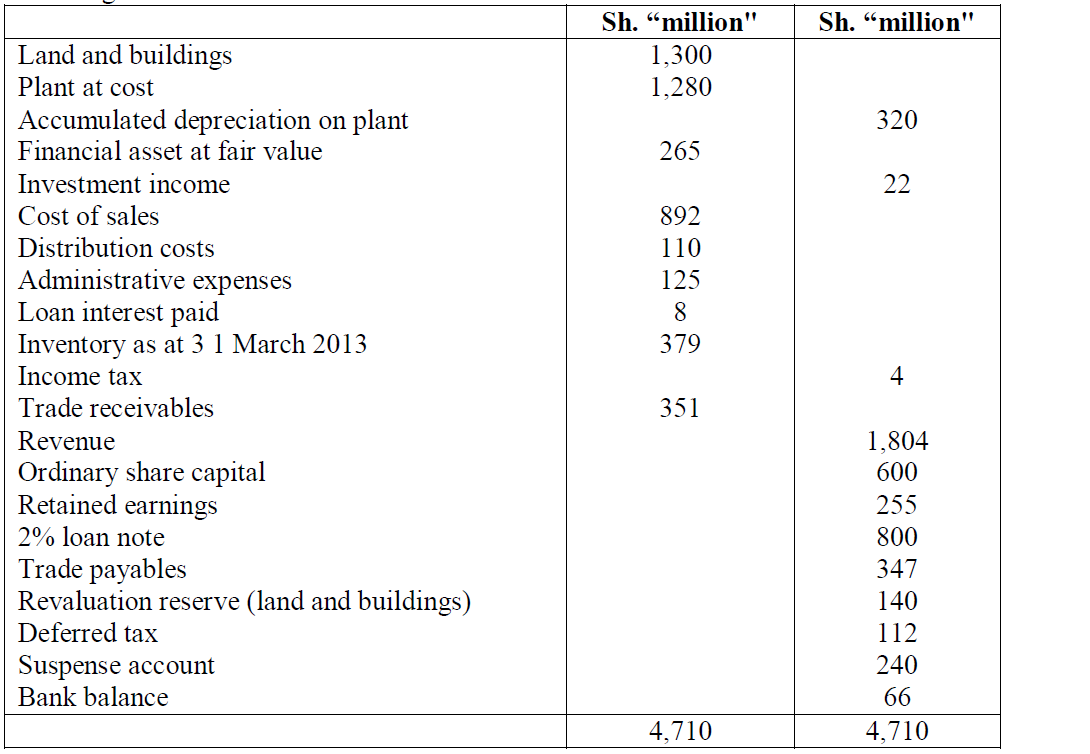

The following trial balance relates to Ndovu Limited as at 31 March 2013:

Additional information:

1. The value of land in the trial balance is given as Sh.300 million. The buildings were revalued on 31 March 2013 at Sh.920 million. The estimated useful life of buildings was 20 years as at 1 April 2012. Depreciation on buildings is charged at 60% to cost of sales and 20% each to distribution costs and administrative expenses.

2. The company constructed its own plant at a total cost of Sh.240 million. The plant was brought into use on 1 October 2012 but its cost had not been capitalized. Instead, its cost had been included in the cost of sales. Plant is depreciated at 12.5% per annum using the reducing balance method (time apportioned) and charged to the cost of sales.

3. The fair value of the investments held at fair value was Sh.271 million as at 3 1 March 2013.

4. The balance of tax on the trial balance represents an overprovision of previous years" tax.

The estimate of tax for the current year is Sh.187 million. At 31 March 2013, there were Sh.400 million of taxable temporary differences. For deferred, tax assume an average tax rate of 30%.

5. The 2% loan note was issued on 1 October 2012 under the terms that require a large premium on repayment. The effective interest rate therefore is 6% per annum.

6. The suspense account relates to a rights issue of shares that was made on 1 January 2013. The terms of the issue were one share for every four held at Sh.8 per share. The par value of each share is Sh.5. The issue was fully subscribed.

Required:

Prepare the following statements in a format suitable for publication:

a) Statement of comprehensive income for the year ended 31 March 2013.

b) Statement of financial position as at 31 March 2013.

Additional information:

1. The value of land in the trial balance is given as Sh.300 million. The buildings were revalued on 31 March 2013 at Sh.920 million. The estimated useful life of buildings was 20 years as at 1 April 2012. Depreciation on buildings is charged at 60% to cost of sales and 20% each to distribution costs and administrative expenses.

2. The company constructed its own plant at a total cost of Sh.240 million. The plant was brought into use on 1 October 2012 but its cost had not been capitalized. Instead, its cost had been included in the cost of sales. Plant is depreciated at 12.5% per annum using the reducing balance method (time apportioned) and charged to the cost of sales.

3. The fair value of the investments held at fair value was Sh.271 million as at 3 1 March 2013.

4. The balance of tax on the trial balance represents an overprovision of previous years" tax.

The estimate of tax for the current year is Sh.187 million. At 31 March 2013, there were Sh.400 million of taxable temporary differences. For deferred, tax assume an average tax rate of 30%.

5. The 2% loan note was issued on 1 October 2012 under the terms that require a large premium on repayment. The effective interest rate therefore is 6% per annum.

6. The suspense account relates to a rights issue of shares that was made on 1 January 2013. The terms of the issue were one share for every four held at Sh.8 per share. The par value of each share is Sh.5. The issue was fully subscribed.

Required:

Prepare the following statements in a format suitable for publication:

a) Statement of comprehensive income for the year ended 31 March 2013.

b) Statement of financial position as at 31 March 2013.

Date posted:

February 14, 2019

-

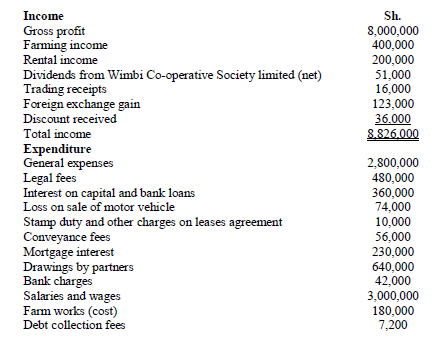

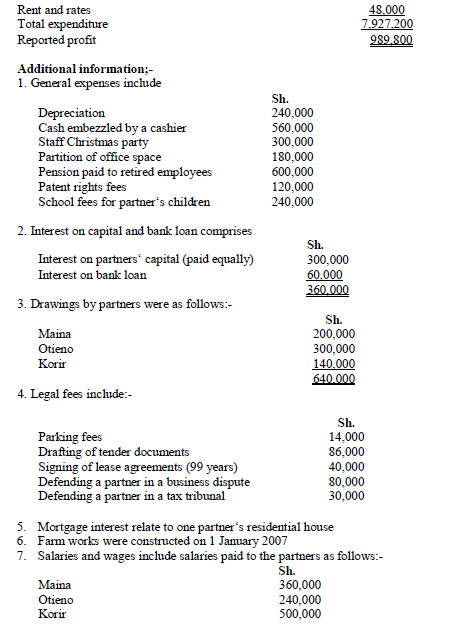

Maina, Otieno and Korir are in a partnership trading as Moko enterprises and sharing profits and losses in the ratio of 2:2:1 respectively

The following income statements was prepared by the partnership for the year ended 31 December 2007

Determine:

i. Adjusted taxable profit or loss of the partnership for the year ended 31 December 2007

ii. A schedule showing the taxable income of each partner for the year ended December 2007

Determine:

i. Adjusted taxable profit or loss of the partnership for the year ended 31 December 2007

ii. A schedule showing the taxable income of each partner for the year ended December 2007

Date posted:

February 14, 2019

-

List four types of dividend income which are exempted from tax in your country

Date posted:

February 14, 2019

-

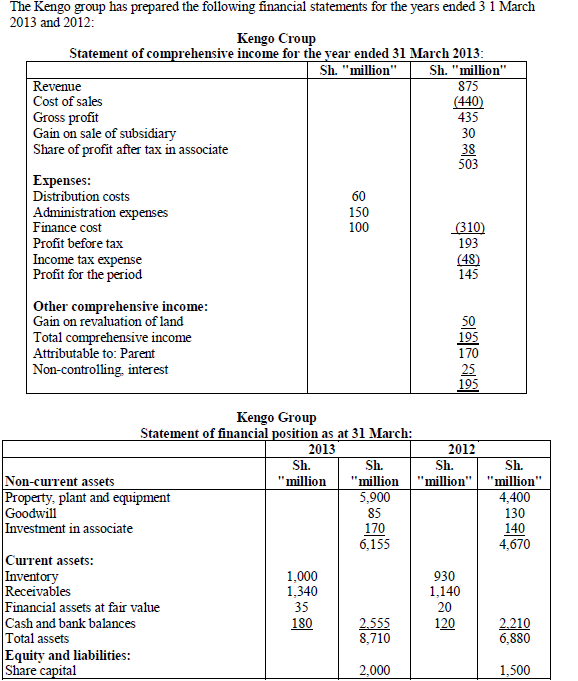

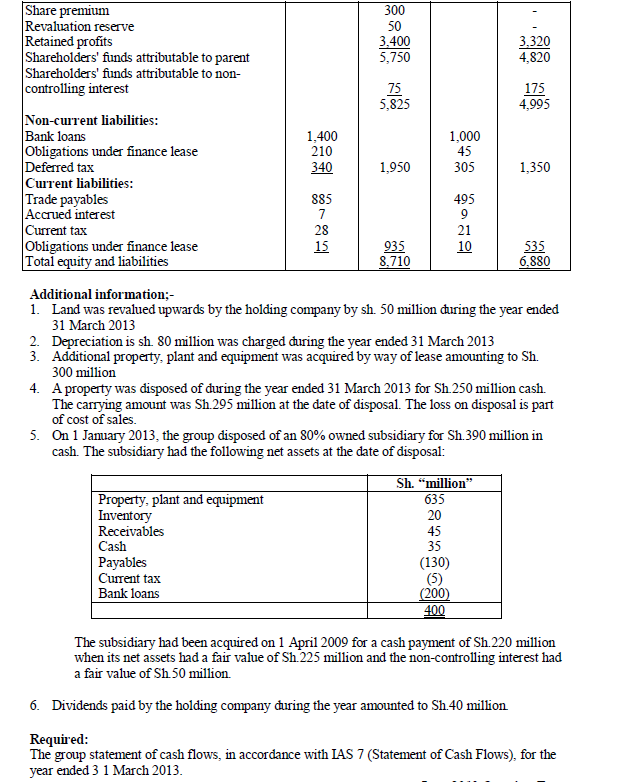

The Kengo group has prepared the following financial statements for the years ended 31st March 2013 and 2012:

Date posted:

February 14, 2019

-

Mr. Ayub Simuyu is a senior manager with Lipa Enterprises limited. He is based at the company‘s headquarters in Nairobi

Mr. Ayub Simuyu has provided the following information on his employment and other income for the year ended 31 December 2007

Determine:

i. Taxable income of Mr. Mr. Ayub Simuyu for the year ended 31 December 2007

ii. Tax payable on the income computed in (i) above

Determine:

i. Taxable income of Mr. Mr. Ayub Simuyu for the year ended 31 December 2007

ii. Tax payable on the income computed in (i) above

Date posted:

February 14, 2019

-

The following trial balance relates to Mapema Limited, a quoted company, as at 30 April 2013:

Required:

Prepare for publication purposes:

a) A statement of comprehensive income for the year ended 30 April 2013.

b) A statement of changes in equity for the year ended 30 April 2013.

c) A statement of financial position as at 30 April 2013.

Required:

Prepare for publication purposes:

a) A statement of comprehensive income for the year ended 30 April 2013.

b) A statement of changes in equity for the year ended 30 April 2013.

c) A statement of financial position as at 30 April 2013.

Date posted:

February 14, 2019

-

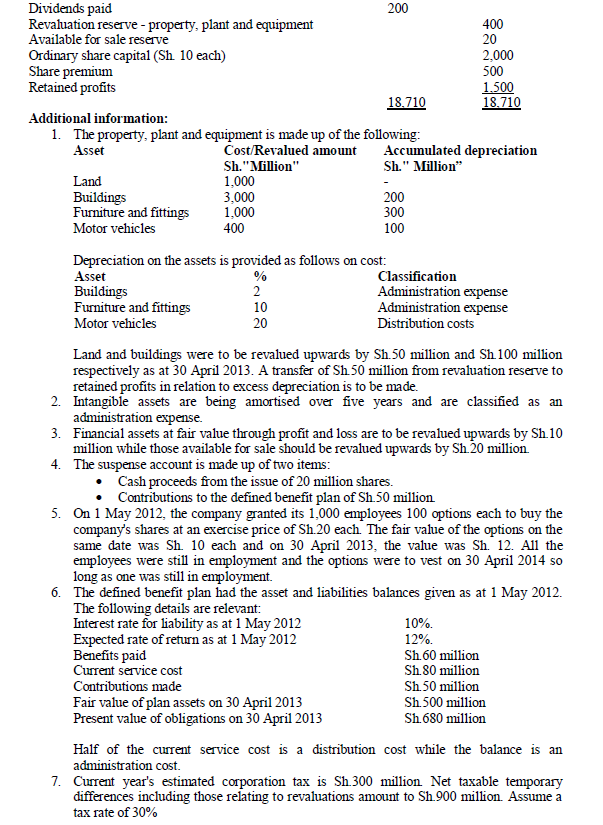

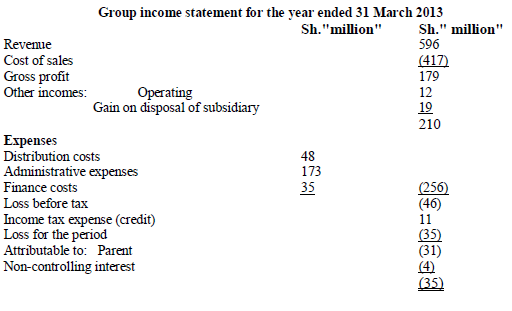

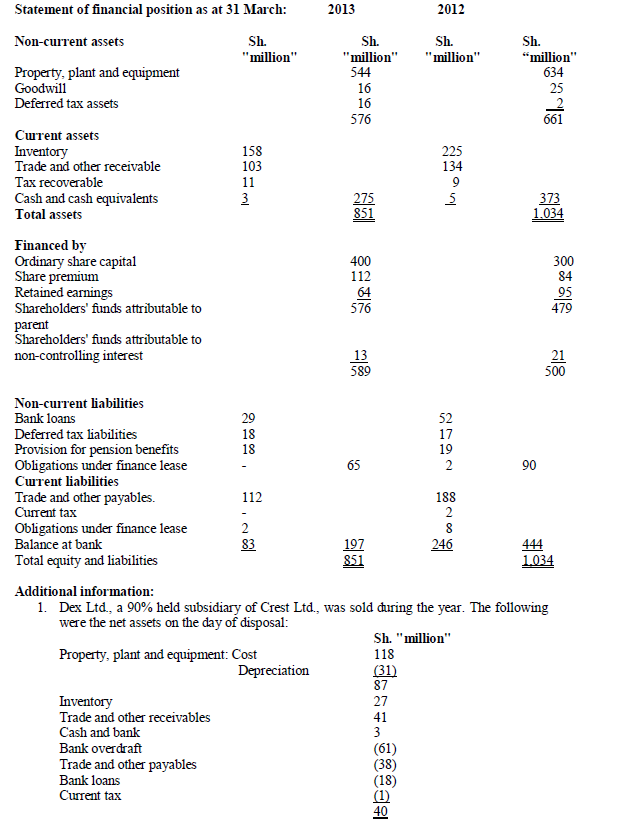

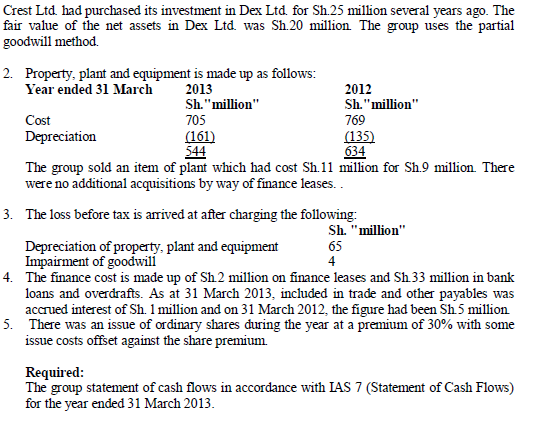

The following financial statements relate to the Crest group for the year ended 31 March 2013:

Date posted:

February 14, 2019

-

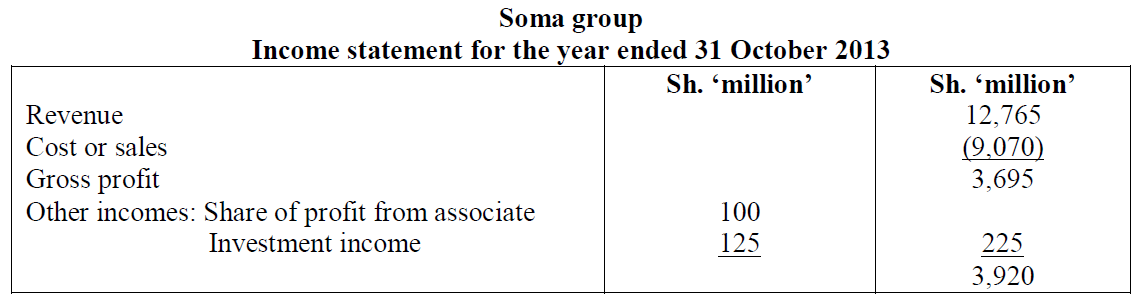

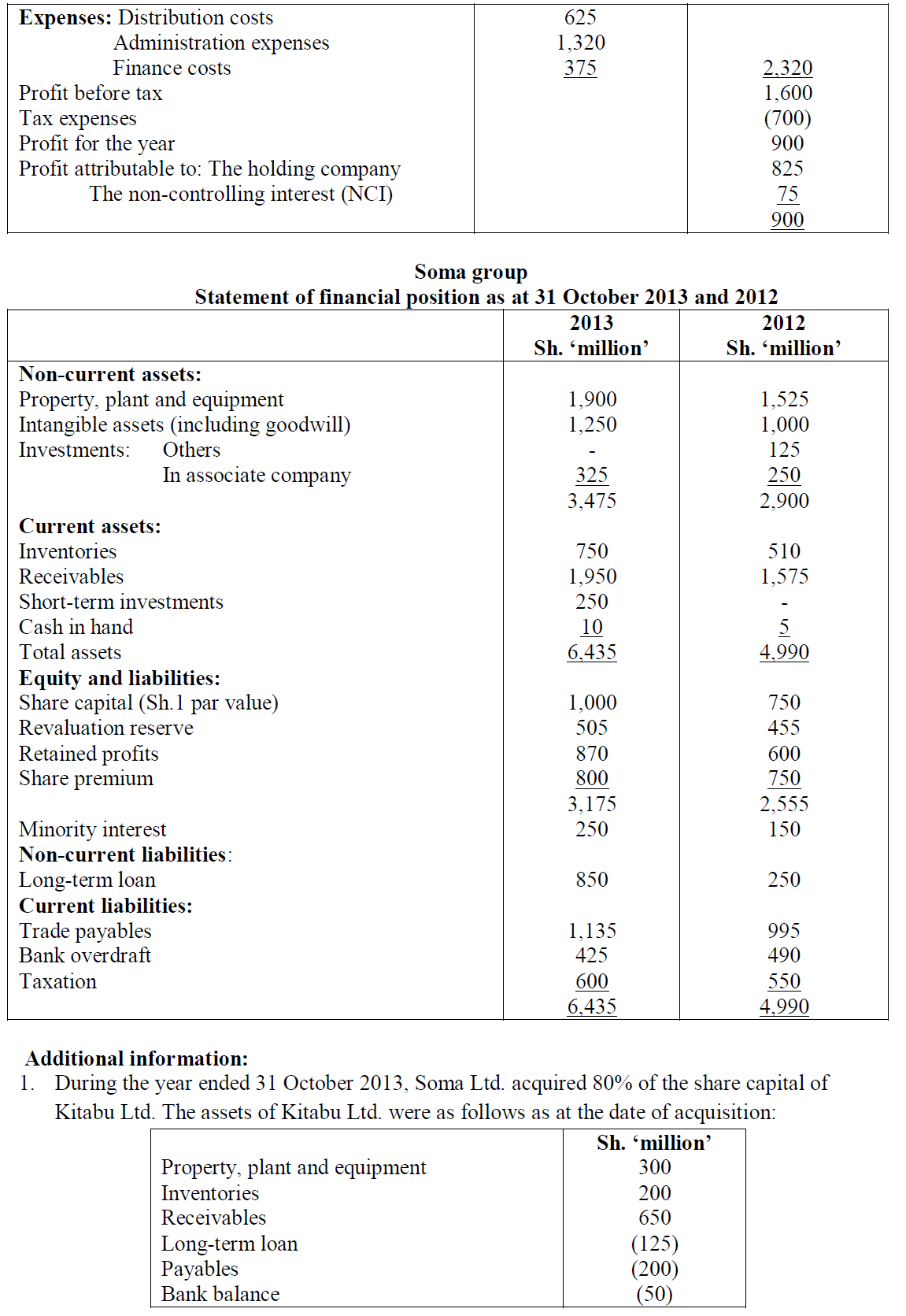

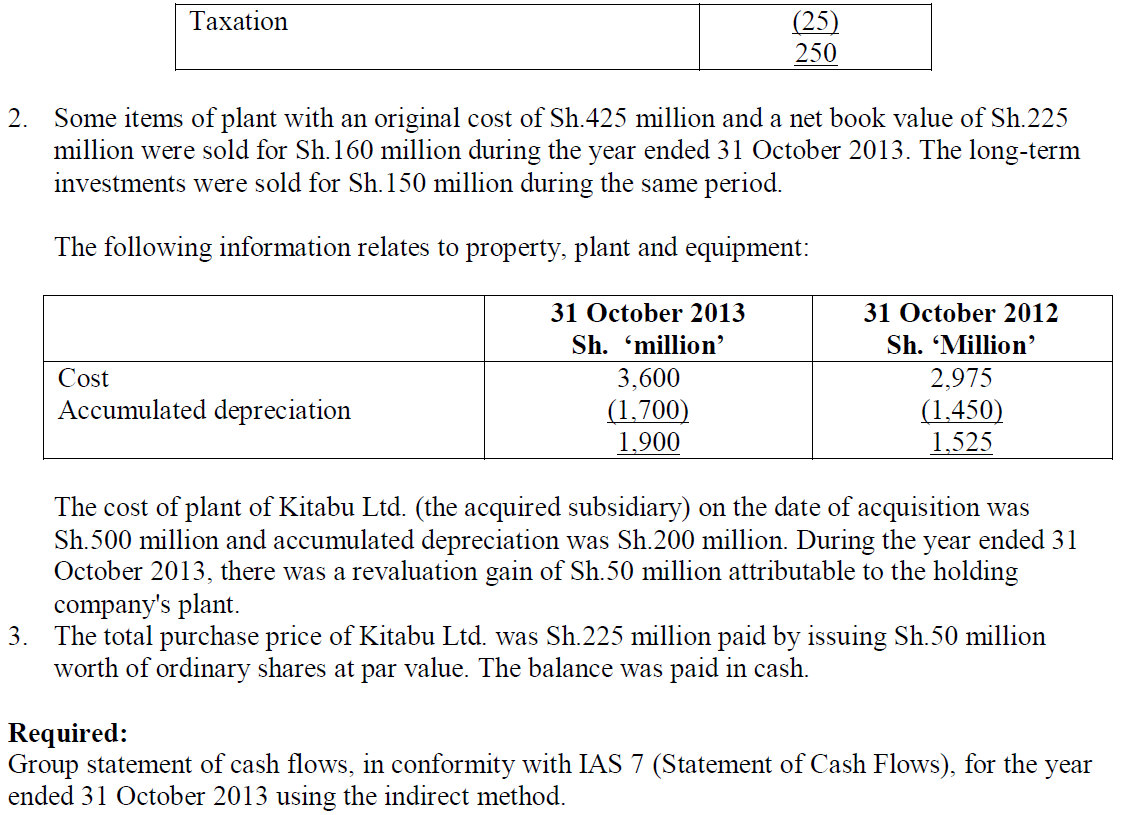

The following are the group income statement and group statement or financial position of Soma group of companies, for the financial year ended 31 October 2013:

Date posted:

February 14, 2019

-

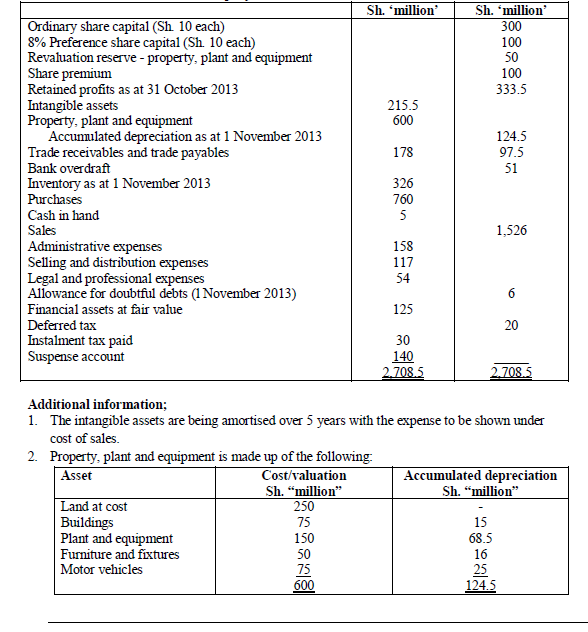

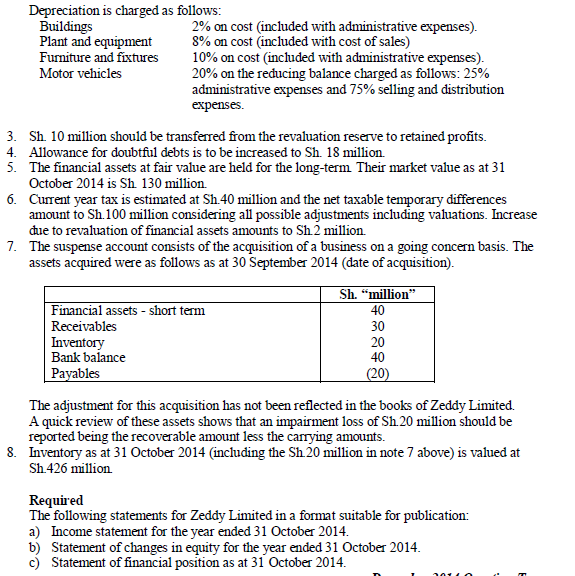

Zeddy Limited is a company quoted at the securities exchange. The following trial balance was extracted from the books of the company as at 31 October 2014:

Date posted:

February 14, 2019

-

Explain the meaning of the following terms as used in pension accounts

(i) Funded schemes.

(ii) Experience adjustments.

Date posted:

February 14, 2019

-

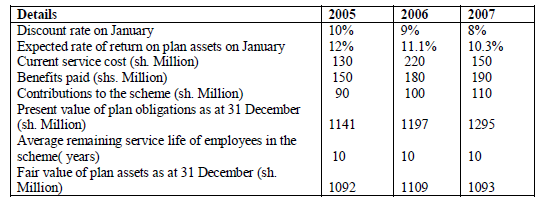

The following relates to Waastaafu Retirement Benefits Scheme, a defined benefit plan, for the years ended 31 December 2005, 2006, and 2007:

Additional information:

1. As at 1 January 2005, the present value of plan obligations and fair value of plan assets were both sh. 1000 million.

2. Net cumulative unrecognized actuarial gains as at 1 January 2005 were sh. 140 million.

3. Assume all transactions occurred at the year end.

Required:

i) Actuarial gains or losses on the present value of plan obligations.

ii) Actuarial gains or losses on fair value of plan assets.

iii) Net pension cost to be charged in the income statement.

iv) Scheme balances to be reflected in the balance sheet

Additional information:

1. As at 1 January 2005, the present value of plan obligations and fair value of plan assets were both sh. 1000 million.

2. Net cumulative unrecognized actuarial gains as at 1 January 2005 were sh. 140 million.

3. Assume all transactions occurred at the year end.

Required:

i) Actuarial gains or losses on the present value of plan obligations.

ii) Actuarial gains or losses on fair value of plan assets.

iii) Net pension cost to be charged in the income statement.

iv) Scheme balances to be reflected in the balance sheet

Date posted:

February 14, 2019

-

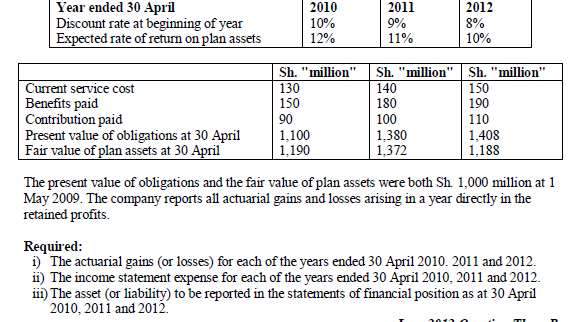

Zedkey Ltd. operates a defined benefit pension plan The following financial data relates to the scheme for the past three years ended 30 April 2012:

Date posted:

February 14, 2019