-

State the factors that the external auditor should consider before placing reliance on the work of the internal auditor

Date posted:

February 22, 2019

-

Explain five circumstances under which an auditor can disclose information to an appropriate authority without client‘s permission

Date posted:

February 22, 2019

-

Outline the ways in which an auditor may be held criminally liable in the course of his audit duties

Date posted:

February 22, 2019

-

In the context of the Companies Act (Cap. 486), outline the procedure for the removal of an auditor

Date posted:

February 22, 2019

-

State and briefly explain an auditor‘s responsibilities with regard to the detection of errors and frauds

Date posted:

February 22, 2019

-

Identify and briefly explain any four inherent limitations of an internal control system

Date posted:

February 22, 2019

-

Explain five factors to consider when preparing a sales forecast for a cash budget.

Date posted:

February 22, 2019

-

Identify and briefly explain four situations under which an auditor would consider qualification of his audit report

Date posted:

February 22, 2019

-

Outline three differences between budgets and standards.

Date posted:

February 22, 2019

-

Differentiate between the following types of budgets

i) Functional budget and master budget.

ii) Rolling budget and incremental budget.

Date posted:

February 22, 2019

-

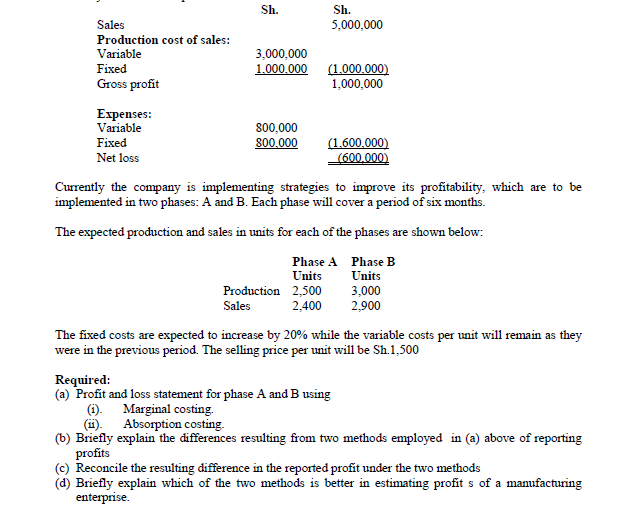

XYZ Ltd. Carries on its business in Nairobi. The company has been reporting its profits using

absorption costing system. During the financial year ended 30 September 2005, the following

summary statement was provided:

Date posted:

February 22, 2019

-

Clearly outline the statutory responsibilities of an external auditor in relation to the audit of a company‘s financial statements

Date posted:

February 22, 2019

-

Identify five audit benefits that could be derived from using Computer Assisted Audit Techniques (CAATs) when carrying out testing of computer records

Date posted:

February 22, 2019

-

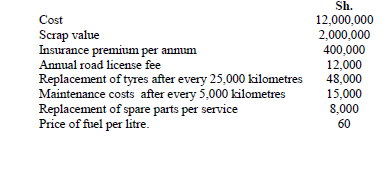

Jogi Transporters operate in the transport industry. On 1 December 2005, the management

acquired a new lorry to meet customer needs and cater for the increase in business volume.

The following information relates to the initial and maintenance cost of the lorry.

Additional information:

1. The lorry has an economic life of 4 years.

2. The lorry has 6 tyres after each costing Sh.8000

3. Service is carried out after every 5,000 kilometres.

4. On average the lorry covers 20 kilometres per litre of fuel consumed.

5. The lorry is projected to cover 100,000 kilometres in January 2006, 25,000 kilometres in

Required:

Prepare a schedule for the three months showing

i. Variable costs per kilometer

ii. Fixed costs per kilometer

iii. Total costs per kilometer

c) Fixed costs are actually variable cost

With reference to (b) above explain whether you agree or disagree with the statement.

February 2006 and 50,000 kilometres in March 2006.

Additional information:

1. The lorry has an economic life of 4 years.

2. The lorry has 6 tyres after each costing Sh.8000

3. Service is carried out after every 5,000 kilometres.

4. On average the lorry covers 20 kilometres per litre of fuel consumed.

5. The lorry is projected to cover 100,000 kilometres in January 2006, 25,000 kilometres in

Required:

Prepare a schedule for the three months showing

i. Variable costs per kilometer

ii. Fixed costs per kilometer

iii. Total costs per kilometer

c) Fixed costs are actually variable cost

With reference to (b) above explain whether you agree or disagree with the statement.

February 2006 and 50,000 kilometres in March 2006.

Date posted:

February 22, 2019

-

State the limitations of break – even analysis.

Date posted:

February 22, 2019

-

Briefly explain how an audit firm may use third party confirmations to provide evidence in relation to six difference balance sheet items

Date posted:

February 22, 2019

-

List four advantages and four disadvantages of using the risk-based audit approach when auditing the financial statements of limited companies

Date posted:

February 22, 2019

-

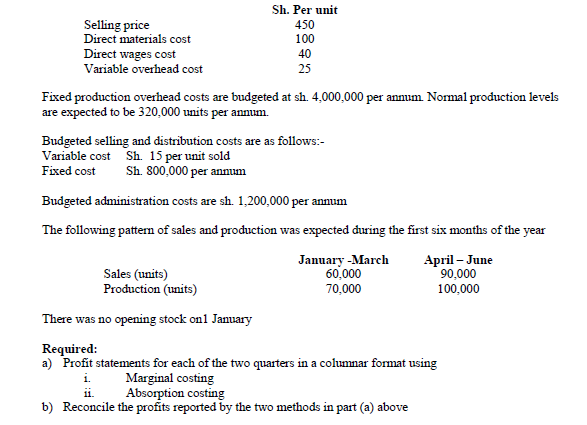

ABC limited manufactures and sells a single product branded 'Zed'. The following data has been

extracted from the budgets and standard costs to product 'Zed'.

Date posted:

February 22, 2019

-

State and briefly explain the action auditors should take if the management refuses to provide a letter of representation.

Date posted:

February 22, 2019

-

Explain the nature and purpose of a post-audit review

Date posted:

February 22, 2019

-

Highlight six limitations of cost-volume-profit analysis.

Date posted:

February 22, 2019

-

Distinguish between a procedural audit and a balance sheet audit

Date posted:

February 22, 2019

-

Describe the difference between the accountant's and the economist's model of cost-volume profit

analysis.

Date posted:

February 22, 2019

-

Explain how Jesus fulfilled the psalmist prophecy about the messiah

Date posted:

February 22, 2019

-

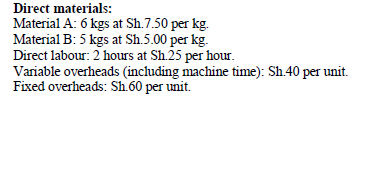

Tec Ltd. manufactures a single product branded 'Zed' for sale on the local and international

market.

The cost structure per unit of product "'zed' is as follows:

Additional information:

1. The current sales level for the company amounts to Sh. 800,000.

2. The fixed overheads per unit have been calculated based on the current sales level of 4,000

units.

Required:

i) Sales price per unit.

ii) Current profit or loss.

iii) Break even point in units and shillings.

iv) Suggest four measures that could be taken to improve the current profit position

Additional information:

1. The current sales level for the company amounts to Sh. 800,000.

2. The fixed overheads per unit have been calculated based on the current sales level of 4,000

units.

Required:

i) Sales price per unit.

ii) Current profit or loss.

iii) Break even point in units and shillings.

iv) Suggest four measures that could be taken to improve the current profit position

Date posted:

February 21, 2019

-

State the observation made in the combustion tube during preparation of ammonia

Date posted:

February 21, 2019

-

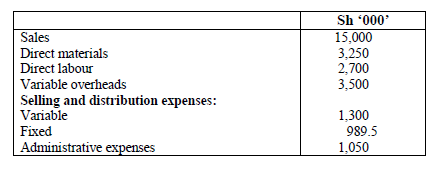

Sifa Ltd. manufactures and sells a single product. The following information regarding the

company for the year ended 31 October 2014 is provided:

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

The following changes are expected to occur during the year ending 31 October 2015:

1. Variable selling and distribution expenses will reduce by 5% due to increased efficiency of the

sales staff.

2. Variable overheads will increase by 3%.

3. Labour cost will reduce by 4%.

4. Material cost will increase by 2% due to inflation.

5. Selling price will reduce by 3% in order to attract customers.

6. No stock is expected at the end of the period.

Required;-

i) Expected break even sales for the year ending 31 October 2015.

ii) Expected margin of safety in sales value for the year ending 31 October 2015.

iii) Expected sales value at which a profit of Sh.2, 250,000 will be realised.

iv) A summary of the operating statement to show net profit in (b) (iii) above.

Date posted:

February 21, 2019

-

List three disadvantages of using standardized audit programmes and how these disadvantages can be avoided.

Date posted:

February 21, 2019

-

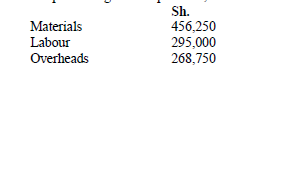

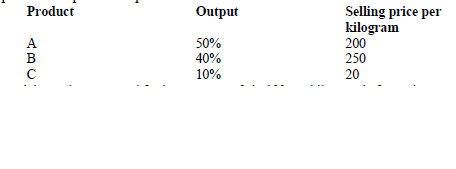

Jitegemee limited company uses a process costing system in its operation. In one of the

production processes, two joint products A and B and a by-product C are produced

The following additional information is provided:

1. Each processing run requires 12,500 kilograms of output.the costs incurred are as follow:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

2. It is expected that 20% of the input will be damaged in the production process. This is sold as

scrap at sh. 10 per kilogram. The damaged items are detected at the end of the production

process.

3. The output from the production process is as follows:-

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

4. Product A has to be processed further at a cost of sh. 100 per kilogram before sale

5. The joint costs are allocated to the products on the basis of net releasable value

Required:

i. Determine the total cost of the output from the production process

ii. Calculate the allocated joint costs for product A and product B

iii. Prepare a process account for the production process above

Date posted:

February 21, 2019

-

Under what circumstances is one ineligible for appointment as an auditor of a company?

Date posted:

February 21, 2019