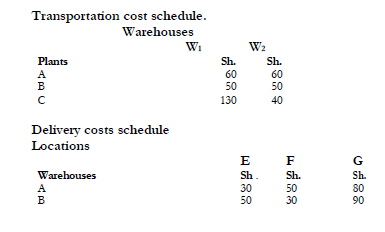

- Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may...(Solved)

Best Sell Ltd. has decided to launch a new product in addition to its range of

products. The following information is available:

1. The new product may be distributed through any combination of the two

company warehouses W1 and W2.

2. The available monthly production capabilities for the new products are:

1000 units at plant A

2000 units at plant B

1000 units at plant C

3. Three major concentration points of customer demand are at locations E, F

and G which are estimated to have a monthly demand of:

900 units at E

800 units at F

900 units at G

4. The unit production costs amount to Sh.30, Sh.40, Sh.10 at A, B and C

respectively.

5. The unit handling costs at the warehouses amount to Sh.20 and Sh.30 at W1

and W2.

6. The unit transportation costs from plant to warehouse and unit delivery cost

from warehouse to customers are as shown below:

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Required:

Determine the optimum production and distribution schedule to minimize total cost.

Date posted: May 7, 2021.

- Explain the following terms as applied in competitive situations:

i) Degeneracy

ii) Pure strategy

iii) Mixed strategy

iv) Dominance rule(Solved)

Explain the following terms as applied in competitive situations:

i) Degeneracy

ii) Pure strategy

iii) Mixed strategy

iv) Dominance rule

Date posted: May 7, 2021.

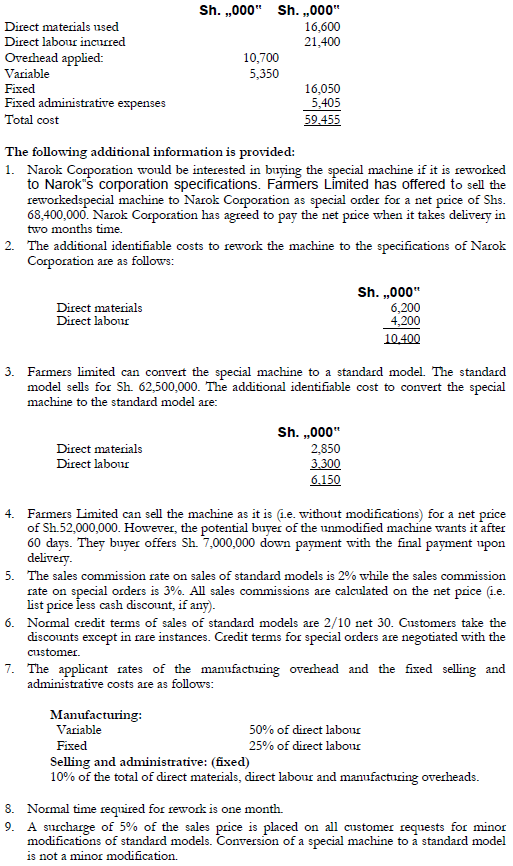

- Farmers Limited had received an order for a piece of special machine from Naivasha

Flowers Limited. Just as farmers completed the machine, Naivasha Flowers Limited was

declared...(Solved)

Farmers Limited had received an order for a piece of special machine from Naivasha

Flowers Limited. Just as farmers completed the machine, Naivasha Flowers Limited was

declared bankrupt, defaulted on the order, and forfeited 10% deposit paid on the selling

price of Sh. 72,000,000. Farmers Limited engineering department manager identified the

costs already incurred in the production of the special machine for Naivasha Flowers limited

as follows:

10. Farmers Limited normally sells a sufficient number of standard models for the company

to operate at a volume in excess of a breakeven point.

11. Farmers Limited does not consider the time value of money in the analysis of special

orders and projects whenever the time period is less than one year because the effect is

not significant.

Required:

(a) Determine the total contribution in shillings for each of the three alternatives

(b) If Narok Corporation makes a counter offer, what is the lowest price farmers

limited should accept for the reworked machine from Narok Corporation?

Explain your answer.

(c) Discuss the influence that fixed factory overhead costs should have on the sales

quoted by Farmers Limited for special orders when:

(i) A firm is operation at or below the breakeven point

(ii) A firm‟s special orders constitute efficient utilization of unused

capacity above the breakeven volume.

10. Farmers Limited normally sells a sufficient number of standard models for the company

to operate at a volume in excess of a breakeven point.

11. Farmers Limited does not consider the time value of money in the analysis of special

orders and projects whenever the time period is less than one year because the effect is

not significant.

Required:

(a) Determine the total contribution in shillings for each of the three alternatives

(b) If Narok Corporation makes a counter offer, what is the lowest price farmers

limited should accept for the reworked machine from Narok Corporation?

Explain your answer.

(c) Discuss the influence that fixed factory overhead costs should have on the sales

quoted by Farmers Limited for special orders when:

(i) A firm is operation at or below the breakeven point

(ii) A firm‟s special orders constitute efficient utilization of unused

capacity above the breakeven volume.

Date posted: May 7, 2021.

- Industrial Chemical Ltd. (ICL) produces chemical Y. the standard ingredients of 1 kilogram

of Y are:

0.65 kilograms of ingredient F @ Sh. 40 per Kg

0.30 kilograms...(Solved)

Industrial Chemical Ltd. (ICL) produces chemical Y. the standard ingredients of 1 kilogram

of Y are:

0.65 kilograms of ingredient F @ Sh. 40 per Kg

0.30 kilograms of ingredient D @ Sh. 60 per Kg.

0.20 kilograms of ingredient N @ Sh. 25 per Kg.

The following additional information is provided:

1. Production of 4,000 kilograms of chemical Y was budgeted for October 2004.

2. The production of chemical Y is entirely automated and production costs attributed to

its production comprise only direct materials and overheads.

3. ICL‟s production process works on a just-in-time (JIT) inventory system and

no ingredients or inventories of chemical Y are held.

4. Overheads budgeted for the production of Y in the month of October 2004 were as

follows:

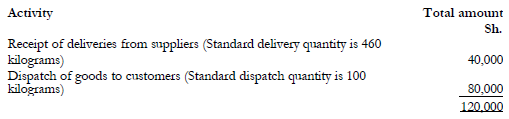

5. In October 2004, 4,200 kilograms of Y were produced and the cost details were as

follows:

Materials used

2,840 kilograms of F, 1,210 kilograms of D and 860 kilograms of N at a total cost of

Sh. 203,800.

Actual overhead costs

12 supply deliveries at a cost of Sh.48,000 and 38 customer dispatches at a cost of

Sh. 78,000 were made.

6. ICL‟s budget committee met recently to discuss the preparation of the cost

control report for October 2004 and the following discussion took place:

Chief accountant: “the overheads do not vary directly worth output and

are therefore by definition „fixed‟. They should be analyzed and reported

accordingly”.

Management accountant: “the overheads do not vary with output, but they

are certainly not fixed. They should be analyzed and reported on an activity based

basis.”

Required:

Having regard to this discussion,

a) Prepare a variance analysis of the production costs of Y in October 2004. (Separate the

material cost variance into price, mixture and yield components and the overhead cost

variance into expenditure, capacity and efficiency components using consumption of

ingredient F as the overhead absorption base).

b) Prepare a variance analysis of the overhead production costs on Y in October 2004 on

an activity based basis.

5. In October 2004, 4,200 kilograms of Y were produced and the cost details were as

follows:

Materials used

2,840 kilograms of F, 1,210 kilograms of D and 860 kilograms of N at a total cost of

Sh. 203,800.

Actual overhead costs

12 supply deliveries at a cost of Sh.48,000 and 38 customer dispatches at a cost of

Sh. 78,000 were made.

6. ICL‟s budget committee met recently to discuss the preparation of the cost

control report for October 2004 and the following discussion took place:

Chief accountant: “the overheads do not vary directly worth output and

are therefore by definition „fixed‟. They should be analyzed and reported

accordingly”.

Management accountant: “the overheads do not vary with output, but they

are certainly not fixed. They should be analyzed and reported on an activity based

basis.”

Required:

Having regard to this discussion,

a) Prepare a variance analysis of the production costs of Y in October 2004. (Separate the

material cost variance into price, mixture and yield components and the overhead cost

variance into expenditure, capacity and efficiency components using consumption of

ingredient F as the overhead absorption base).

b) Prepare a variance analysis of the overhead production costs on Y in October 2004 on

an activity based basis.

Date posted: May 7, 2021.

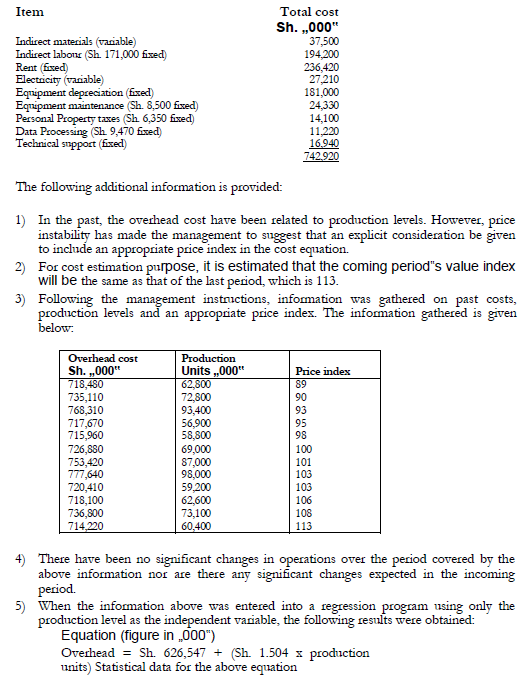

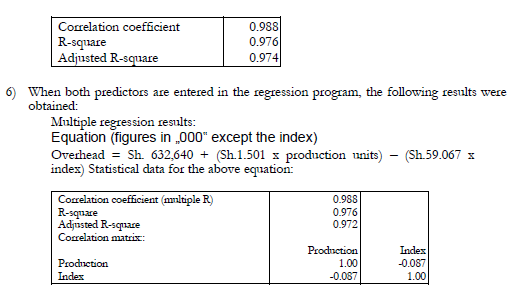

- Maisha Meta Products Ltd. has prepared a schedule of estimated overhead costs for the

coming year. The schedule was prepared on the assumption that production would...(Solved)

Maisha Meta Products Ltd. has prepared a schedule of estimated overhead costs for the

coming year. The schedule was prepared on the assumption that production would amount

to 800,000 units. Costs have been classified as either fixed or variable according to the

judgement of the financial controller. The following overhead cost items and their

classification as either fixed or variable form the basis for the overhead cost schedule:

Required:

a) Determine the cost estimation equation using the account analysis method

b) Use the high-low method to estimate the cost of 800,000 units of production expected

in the coming period.

c) Using the simple linear regression, estimate the cost of 800,000 units of production.

d) Use the multiple regression results to prepare an estimated cost for the 800,000 units in

the incoming period.

e) Comment on which of the methods is more appropriate under the above circumstances.

Required:

a) Determine the cost estimation equation using the account analysis method

b) Use the high-low method to estimate the cost of 800,000 units of production expected

in the coming period.

c) Using the simple linear regression, estimate the cost of 800,000 units of production.

d) Use the multiple regression results to prepare an estimated cost for the 800,000 units in

the incoming period.

e) Comment on which of the methods is more appropriate under the above circumstances.

Date posted: May 6, 2021.

- Various attempts have been made in the public sector to achieve a more stable, long-term

planning base in contrast to the traditional short-term annual budgeting approach,...(Solved)

Various attempts have been made in the public sector to achieve a more stable, long-term

planning base in contrast to the traditional short-term annual budgeting approach, with its

emphasis on flexibility.

Required:

(a) Explain the deficiencies of the traditional approach to planning which led to the

attempts to introduce planning programming budgeting system (PPBS).

(b) Give an illustration of how PPBS plan could be drawn up in respect of one sector

of public authority activity.

(c) Discuss the problems which have made it difficult in practice to introduce PPBS.

Date posted: May 6, 2021.

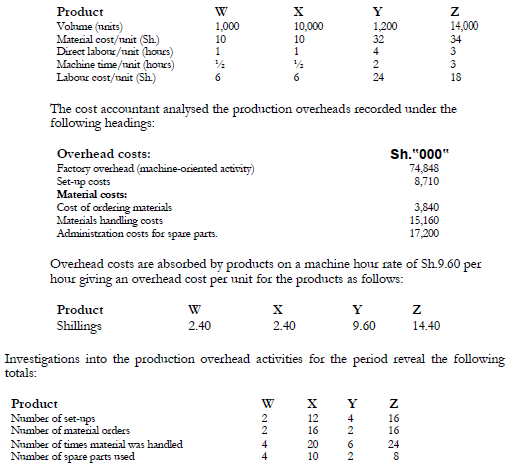

- The Marima Manufacturing Company produces four products; W, X, Y and Z using

the same plant and processes.

The following information relates to the company:

Required:

(i) Unit costs...(Solved)

The Marima Manufacturing Company produces four products; W, X, Y and Z using

the same plant and processes.

The following information relates to the company:

Required:

(i) Unit costs per product using activity-based costing tracing costs to production units by

means of cost drivers.

(ii) Comment briefly on the differences disclosed between overheads traced by the present

system and those traced by activity based costing.

Required:

(i) Unit costs per product using activity-based costing tracing costs to production units by

means of cost drivers.

(ii) Comment briefly on the differences disclosed between overheads traced by the present

system and those traced by activity based costing.

Date posted: May 6, 2021.

- The current thinking in Management Accounting contends that Activity-Based

Costing (ABC) provides better information concerning products costs and decision

making than traditional management accounting techniques.

However, whereas ABC...(Solved)

The current thinking in Management Accounting contends that Activity-Based

Costing (ABC) provides better information concerning products costs and decision

making than traditional management accounting techniques.

However, whereas ABC may give a different impression of product costs, it is not

necessarily a good idea and it may be advisable to continue improving traditional

cost accounting techniques before moving to ABC.

Required:

(i) Explain cost behaviour issues underlying the use of ABC.

(ii) Explain why ABC might, be more suitable for modern manufacturing

environment than traditional cost accounting techniques?

(iii) Comment on the reported claim that ABC gives better information as a

guide to decision making than the traditional product costing techniques.

Date posted: May 6, 2021.

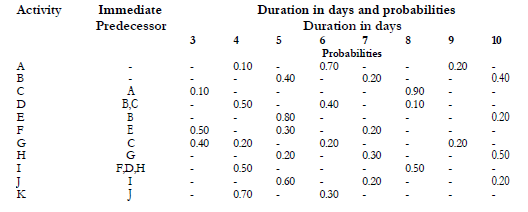

- Mwamba Development Group (MDG) plans to undertake a project consisting of eleven (11)

tasks. The expected completion time of each task is uncertain and this makes...(Solved)

Mwamba Development Group (MDG) plans to undertake a project consisting of eleven (11)

tasks. The expected completion time of each task is uncertain and this makes the project

completion time uncertain. MDG has approached a consultancy firm for advice on the

expected project completion time.

The consultancy firm intends to use simulation analysis to deal with the uncertainty of the

project completion time. The following data were obtained by the consultancy firm, for the

purpose of simulation analysis:

Required:

(a) Explain the basic steps that can be used to solve this type of problem simulation

technique.

(b) Draw the network for the project and determine the critical path of the project. Use the

activity‟s expected time to determine the expected completion time of the

project.

(c) Carry out four simulation runs for each activity and using the results of the

simulation, determine the expected project completion time.

(d) State two advantages and two disadvantages of the simulation technique.

Use the following random numbers.

95, 30, 59, 93, 28, 72, 09, 54, 66, 95, 36, 98, 56, 23, 60, 79, 14, 50, 61, 81, 84, 14, 24,

75, 85, 49, 05, 09, 53, 45, 60, 98, 90, 86, 74, 55, 69, 09, 10, 96, 40, 27, 15, 83

Required:

(a) Explain the basic steps that can be used to solve this type of problem simulation

technique.

(b) Draw the network for the project and determine the critical path of the project. Use the

activity‟s expected time to determine the expected completion time of the

project.

(c) Carry out four simulation runs for each activity and using the results of the

simulation, determine the expected project completion time.

(d) State two advantages and two disadvantages of the simulation technique.

Use the following random numbers.

95, 30, 59, 93, 28, 72, 09, 54, 66, 95, 36, 98, 56, 23, 60, 79, 14, 50, 61, 81, 84, 14, 24,

75, 85, 49, 05, 09, 53, 45, 60, 98, 90, 86, 74, 55, 69, 09, 10, 96, 40, 27, 15, 83

Date posted: May 6, 2021.

- Kenya Fashions Ltd. sells a wide range of high quality customized outfits. One

particular outfit is bought at Sh.800 and sold at Sh.1,300. Mean holding costs...(Solved)

Kenya Fashions Ltd. sells a wide range of high quality customized outfits. One

particular outfit is bought at Sh.800 and sold at Sh.1,300. Mean holding costs per

season per outfit amounts to Sh.50 and it costs Sh.8,000 to order and receive goods

into stock. The manufacturers require orders in advance and once a batch has been

made, it is not possible to place a repeat order. Further, it is not possible for

delivery to be staggered over the fashion season.

When a customer buys an outfit, she has a fitting, any alterations or adjustments are

made, and then she collects the outfit a day or so later. Generally if an outfit is out

of stock at one branch, it can be readily obtained from another branch, usually in a

matter of hours. However, if the company as a whole runs out of an item, then the

cost of the stock out is Shs. 200 per item. If the company over buys for a season,

then it is expected that it will be able to dispose of the surplus outfits at Sh.500 each.

The problem facing the management accountant of the company is to decide how many

outfits to order for the season ahead in order to maximize expected profit, bearing in mind

the penalties for over and under ordering.

Required:

(i) Determine the number of outfits to order to maximize expected profits.

(ii) Compare and contrast the model that you have developed with the classical economic

quantity model.

Date posted: May 6, 2021.

- From past experience, a company operating a standard cost accounting system has

accumulated the following information in relation to variances in its monthly

management accounts:

1. Its variances...(Solved)

From past experience, a company operating a standard cost accounting system has

accumulated the following information in relation to variances in its monthly

management accounts:

1. Its variances fall into two categories:

2. For the first category corrective action has eliminated 70% of the variances,

but the remainder have continued unchanged.

3. The cost of an investigation averages Sh.3,500 and that of correcting

variances averages sh.5,500.

4. The average cost of any variance not corrected is Sh.5,250 per month and

the company's policy is to assess the present value of such costs at 2% per

month for a period of five months.

Required:

(i) Two decision trees to represent the position if an investigation is carried

out and the position when an investigation is not carried out.

(ii) Recommend with supporting calculations, whether or not the company

should follow a policy of investigating variances as a matter of routine.

(iii) Explain briefly two types of circumstances that would give rise to variances

in the first category and two types of circumstances that would give rise to

variances in the second category.

2. For the first category corrective action has eliminated 70% of the variances,

but the remainder have continued unchanged.

3. The cost of an investigation averages Sh.3,500 and that of correcting

variances averages sh.5,500.

4. The average cost of any variance not corrected is Sh.5,250 per month and

the company's policy is to assess the present value of such costs at 2% per

month for a period of five months.

Required:

(i) Two decision trees to represent the position if an investigation is carried

out and the position when an investigation is not carried out.

(ii) Recommend with supporting calculations, whether or not the company

should follow a policy of investigating variances as a matter of routine.

(iii) Explain briefly two types of circumstances that would give rise to variances

in the first category and two types of circumstances that would give rise to

variances in the second category.

Date posted: May 6, 2021.

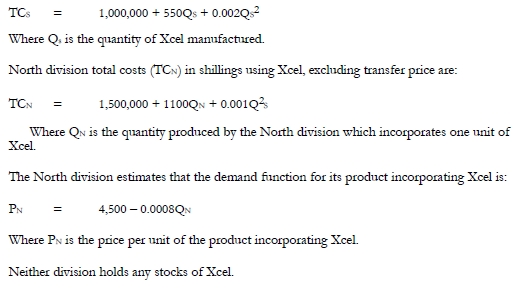

- Nairobi Enterprise Ltd. (NEL) is a divisionalized enterprise. Among its divisions, are South

and North. Both of these divisions have a wide range of independent activities....(Solved)

Nairobi Enterprise Ltd. (NEL) is a divisionalized enterprise. Among its divisions, are South

and North. Both of these divisions have a wide range of independent activities. One

product, Xcel, is made by South division for North division. South division does not have

any external customers for the product.

The central management of NEL delegates all pricing decisions to divisional managers and

the pricing of Xcel has been a contentious issue. It has been suggested that South division

should give a transfer price schedule for the supply of Xcel based on South

division‟s own production costs and that all goods transferred would be made at

South division‟s marginal costs. The North division would then order the quantity it

requires each month. South estimates its monthly total costs (TC) in shillings for producing

Xcel using the following equation:

Required:

(a) (i) The quantity of Xcel which would maximize profits for NEL.

(ii) The transfer price in shillings corresponding to the maximum production in (i)

above if South division‟s marginal cost are adopted for transfer pricing. Show the

resulting profit for each division.

(b) (i) The quantity of Xcel which North division would take (at South division's marginal

costs) if it wanted to maximize its own profits.

(ii)The transfer price in shillings corresponding to the quantity of Xcel that would

maximize the profits of North division, and the resulting profit for each division.

Required:

(a) (i) The quantity of Xcel which would maximize profits for NEL.

(ii) The transfer price in shillings corresponding to the maximum production in (i)

above if South division‟s marginal cost are adopted for transfer pricing. Show the

resulting profit for each division.

(b) (i) The quantity of Xcel which North division would take (at South division's marginal

costs) if it wanted to maximize its own profits.

(ii)The transfer price in shillings corresponding to the quantity of Xcel that would

maximize the profits of North division, and the resulting profit for each division.

Date posted: May 6, 2021.

- State the factors to be taken into consideration when establishing the length of a budget period.(Solved)

State the factors to be taken into consideration when establishing the length of a budget period.

Date posted: May 6, 2021.

- The paradox is that, “while cost plus pricing is devoid of any theoretical justification, it is widely used in practice”.

Discuss the possible justification for its...(Solved)

The paradox is that, “while cost plus pricing is devoid of any theoretical justification, it is widely used in practice”.

Discuss the possible justification for its use.

Date posted: May 6, 2021.

- In preparing the cash budget for the next year, Kericho Tea Farm Limited finds that

it has limited surplus funds of Sh.70,000,000 which the managing directors...(Solved)

In preparing the cash budget for the next year, Kericho Tea Farm Limited finds that

it has limited surplus funds of Sh.70,000,000 which the managing directors wishes

to spend on one of two schemes.

Scheme A - Pay Sh.70,000,000 immediately to reputable sales promotion agency which

would provide extensive advertising and planned „reminder‟ advertising over

the next ten years. This is expected to increase the net operational cash flows

by sh.200,000,000 per annum for the first five years and Sh.100,000,000 for

the following five years. Thereafter, the effect would be zero.

Scheme B - Buy immediately labour saving machinery at a cost of Sh.70,000,000 which

would reduce the operating cash outflows by sh.150,000,000 per annum for

the next ten years, at the end of which the equipment will have a salvage

value of zero.

Required

(i) The average accounting rate of return (ARR) per annum for each scheme over 10 years.

(ii) The net present value (NPV) for each scheme assuming the desired rate of return is 18%.

(iii) The internal rate of return (IRR) for each alternative.

Date posted: May 6, 2021.

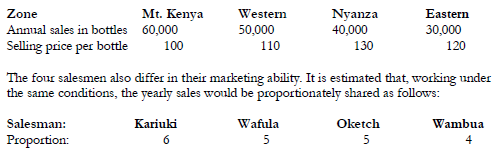

- Marashi Company Ltd. is a merchandising company selling a 40ml bottle of perfume in four

zones within Kenya. The variable cost per bottle is Sh.70 but...(Solved)

Marashi Company Ltd. is a merchandising company selling a 40ml bottle of perfume in four

zones within Kenya. The variable cost per bottle is Sh.70 but the selling price is different in

each of the four zones. The difference in the selling price is due to the transportation costs

involved. The company has four salesmen available for an assignment in the four zones. The

zones are not equally good in their sales potential. It is estimated that a typical salesman

operating in each zone would bring the following annual sales:

The objective of Marashi Company Ltd. is to maximize contribution from each zone.

Required:

(a) Determine how the four salesmen can be assigned to the zones in order for the

company to maximize the total contribution.

(b) Calculate the total contribution of the company after the assignment.

The objective of Marashi Company Ltd. is to maximize contribution from each zone.

Required:

(a) Determine how the four salesmen can be assigned to the zones in order for the

company to maximize the total contribution.

(b) Calculate the total contribution of the company after the assignment.

Date posted: May 6, 2021.

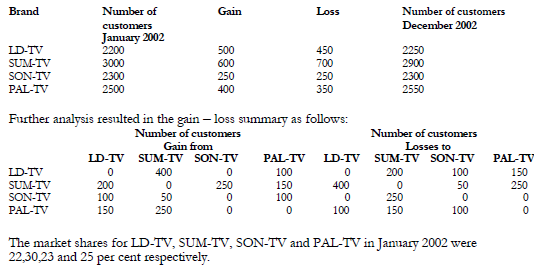

- Nzewani Electronic Ltd. manufactures and sells a brand of television sets called LD-TVs.

The three closest competitor brands in the market are SUM-TVs, SON-TVs. Because of...(Solved)

Nzewani Electronic Ltd. manufactures and sells a brand of television sets called LD-TVs.

The three closest competitor brands in the market are SUM-TVs, SON-TVs. Because of the

custom manufacturing process and their inherent high costs, no other competitor has any

effect on the current market. The year 2002 was an exceptionally good year in terms of gain loss

trade offs. The year's activity is summarized in the following table:

Required:

(a) Advise the management of Nzewani Electronic Ltd. on the expected market share

for each brand at the end of December 2002.

(b) Assuming the same pattern of switching persists, what would be the long run

market share for each brand?

(c) What are the assumptions of the technique you have used in (a) and (b) above?

Required:

(a) Advise the management of Nzewani Electronic Ltd. on the expected market share

for each brand at the end of December 2002.

(b) Assuming the same pattern of switching persists, what would be the long run

market share for each brand?

(c) What are the assumptions of the technique you have used in (a) and (b) above?

Date posted: May 6, 2021.

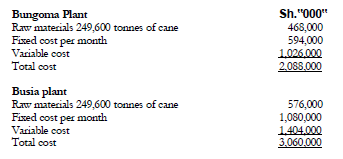

- A sugar manufacturing company has two plants, one in Bungoma and the other one in

Busia, producing equivalent grades of sugar. The Bungoma plant has been...(Solved)

A sugar manufacturing company has two plants, one in Bungoma and the other one in

Busia, producing equivalent grades of sugar. The Bungoma plant has been operating at 75%

of its producing 270,000 tonnes of sugar per month. The Busia plant has been operating at

60% of its capacity producing 360,000 tonnes of sugar per month. The major raw material

used in producing sugar is cane. For each 800 tonnes of sugar, 1000 tonnes of care is

required. At the Bungoma plant, the local cane costs are Sh.1,875 per tonne but the supply is

limited to 144,000 tonnes per month. At Busia plant, local cane costs sh.3000 per tonne and

is limited to 400,000 tonnes per month. Additional cane must be purchased through brokers

at sh.2,750 per tonne (delivered at either plant). The cost schedules for a typical month‟s

production are as follows:

Required:

(a) (i) If the total combined production of both plants is to be maintained at a rate of

630,000 tonnes per month, would there be any apparent advantage in shifting part

of the schedule production from one plant to the other? If so, which plant's

production should be increased and by how much?

(ii) What is the amount of the cost saving as a result of this switch?

(b) If production requirements increased to 910,000 tonnes, how much would you

recommend to be produced at each plant?

Required:

(a) (i) If the total combined production of both plants is to be maintained at a rate of

630,000 tonnes per month, would there be any apparent advantage in shifting part

of the schedule production from one plant to the other? If so, which plant's

production should be increased and by how much?

(ii) What is the amount of the cost saving as a result of this switch?

(b) If production requirements increased to 910,000 tonnes, how much would you

recommend to be produced at each plant?

Date posted: May 6, 2021.

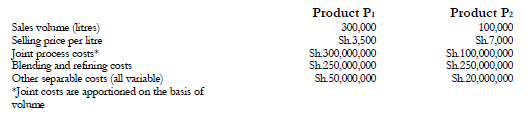

- Sanders Ltd is a manufacturing company producing two joint products P1 and P2 in the ratio

of 3:1 at the split-off point. The two products are...(Solved)

Sanders Ltd is a manufacturing company producing two joint products P1 and P2 in the ratio

of 3:1 at the split-off point. The two products are taken to the mixing plant for blending and

refining after the split off point. The following information is also provided:

The joint process costs are 70% fixed and 30% variable whereas the mixing plant costs are

30% fixed and 70% variable. There are only 5000 hours available in the mixing plant. Usually

4000 hours are taken in processing of Product P1 and P2, 2000 hours for each product while

the remaining 1000 hours are used for other work that generates a contribution of

Sh.100,000 per hour.

The company is now planning to change the production mix of the joint process to 3:2 for

product P1 and P2 respectively. This change will result in an increase in the joint cost by

Sh.500 for each additional litre of P2produced.

Required:

(a) Advise the company on whether to change the production mix.

(b) Explain other qualitative factors that are important to consider before changing the production mix.

The joint process costs are 70% fixed and 30% variable whereas the mixing plant costs are

30% fixed and 70% variable. There are only 5000 hours available in the mixing plant. Usually

4000 hours are taken in processing of Product P1 and P2, 2000 hours for each product while

the remaining 1000 hours are used for other work that generates a contribution of

Sh.100,000 per hour.

The company is now planning to change the production mix of the joint process to 3:2 for

product P1 and P2 respectively. This change will result in an increase in the joint cost by

Sh.500 for each additional litre of P2produced.

Required:

(a) Advise the company on whether to change the production mix.

(b) Explain other qualitative factors that are important to consider before changing the production mix.

Date posted: May 6, 2021.

- Two manufacturers compete in a market for a specialized calculator. Company A

controls 75% of the market while company B controls 25% of the market. Company...(Solved)

Two manufacturers compete in a market for a specialized calculator. Company A

controls 75% of the market while company B controls 25% of the market. Company A

is considering a vigorous annual marketing campaign which will cost Sh.35,000,000. The

total market for the specialize calculator is 100,000 units per year. The profit

contribution per unit is Sh.3,000.

Company B is debating how much money to invest in research and development every

year. It is considering three alternatives: Sh.25,000,000, Sh.50,000,000 and Sh.80,000,000.

It is estimated that if company A runs a vigorous annual marketing campaign, its share

of the market after one yea will be either 79% or 73%, depending on company B‟s

investment in research and development (Sh.25,000,000, 50,000,000 and

Sh.80,000,000 respectively).

On the other hand, if company A does not run the marketing campaign, company

B‟s share of the market will decrease by 1% of the total market if it invests Sh.25,000,000 in

research and development, increase by 1% if it invests Sh.50,000,000 in research and

development and increase by 3% if Sh.80,000,000 is invested.

Required:

i Using the share of the market percentages only, convert the above into a zero sum game, and hence solve for the optimal strategies for both companies.

ii Obtain a pay off table consisting of contribution to profit in monetary terms, and hence solve the game.

Date posted: May 6, 2021.

- Aberdares Company Ltd. is a manufacturing company which produces and sells a single

product known as T1 at a price of Sh.10 per unit. The company...(Solved)

Aberdares Company Ltd. is a manufacturing company which produces and sells a single

product known as T1 at a price of Sh.10 per unit. The company incurs a variable cost of Sh.6

per unit and fixed costs of Sh.400,000. Sales are normally distributed with a mean of 110,000

units and a standard deviation of 10,000 units. The company is considering producing a

second product, T2 to sell at Sh.8 per unit and incur a variable cost of Sh.5 per unit with

additional fixed costs of Sh.50,000. The demand for T2 is also normally distributed with a

mean of 50,000 units and standard deviation of 5,000 units. If T2 is added to the production

schedule, sales of T 1 will shift downwards to a mean of 85,000 units and standard deviation

of 8,000 units. The correlation coefficient between sales of T1 and T2 is – 0.9.

Required:

i The company‟s break-even point for the current and proposed production schedules.

ii The coefficient of variation for the two proposals.

iii Based on your computation‟s in (i) and (ii) above advise the company on whether to add T2 to its production schedule.

Date posted: May 6, 2021.

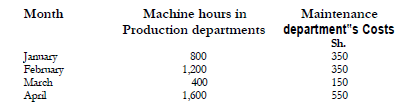

- High-tex Engineering Company Limited wishes to set flexible budgets for each of its operating departments. A separate maintenance department performs all routine and major repair...(Solved)

High-tex Engineering Company Limited wishes to set flexible budgets for each of its operating departments. A separate maintenance department performs all routine and major repair works on the company‟s equipment and facilities. The company has determined that maintenance department performs all routine and major repair works on the

company's equipment and facilities. The company has determined that maintenance cost is

primarily a function of machine hours worked in the various production departments.

The maintenance cost incurred and the actual machine hours worked during the months of

January, February, March and April 2003 were as follows:

Required:

a) Determine the cost estimation function using:

i High-low method.

ii Regression analysis

b) Using the regression function estimate:

i The maintenance costs that would have been incurred if the machine hours were expected to be 900 in the month of May 2003.

ii The maximum machine hours that would have been worked If the maintenance cost incurred had been limited to Sh.400,000 for the month of May 2003.

c) Assuming that in the month of May 2003 machine hours were 900, establish a 95% confidence interval for this point estimate. (Assume tc = 2.7764 and standard error of estimate, se = 63.25).

Required:

a) Determine the cost estimation function using:

i High-low method.

ii Regression analysis

b) Using the regression function estimate:

i The maintenance costs that would have been incurred if the machine hours were expected to be 900 in the month of May 2003.

ii The maximum machine hours that would have been worked If the maintenance cost incurred had been limited to Sh.400,000 for the month of May 2003.

c) Assuming that in the month of May 2003 machine hours were 900, establish a 95% confidence interval for this point estimate. (Assume tc = 2.7764 and standard error of estimate, se = 63.25).

Date posted: May 6, 2021.

- Joan Odero, an independent movie producer, is negotiating with Roadshow Productions

Limited on a contract for the production and marketing of her next film, titled “The

rise...(Solved)

Joan Odero, an independent movie producer, is negotiating with Roadshow Productions

Limited on a contract for the production and marketing of her next film, titled “The

rise and fall of a cock”. The budget for the film is, Sh.100 million.

Roadshow Productions Limited is offering Joan Odero a choice of one of the three contracts.

Contract A

1. Roadshow Productions Limited will pay all the production and marketing costs.

2. Joan Odero will receive a fixed fee of Sh.10 million.

3. Joan Odero will receive 10% of gross revenue from the film in excess of Sh.1 billion

(no payment is made for gross revenue up to Sh.1 billion).

Contract B

1. Roadshow Productions Limited will pay 80% of all the production and marketing costs

up to Sh.100 million and 30% of production and marketing costs in excess of Sh.100 million

2. Joan Odero will receive 10% of all gross revenue for the film. Contract C

1. Roadshow Productions Limited will pay 50% of production and marketing costs up to Sh.100 million.

2. Joan Odero will receive 30% of all gross revenue from the film.

Joan Odero estimates the following probabilities for the gross revenues:

P(high demand of Sh.2 billion) 0.1

P(medium demand of Sh.500 million) 0.3

P(low demand of Sh.100 million) 0.6

She estimates the following probabilities for the cost of production:

P(budgeted cost of Sh.100 million) 0.6

P(high cost of Sh.200 million) 0.4

Required:

a) The expected monetary value for Joan Odero under each contract for each of the six possible events.

(Hint: The possible events are high demand – budgeted costs, high demand –

high costs, medium demand – budgeted costs, medium demand – high costs, low demand – budgeted costs, and low demand – high costs).

b) Joan Odero will choose the contract that maximizes her expected monetary value from the film. Which contract should she choose? (Show calculations).

c) What information might Joan Odero use in assessing the probability distribution for the production and marketing costs of “The rise an fall of cock” film?

Date posted: May 6, 2021.

- Traditional budgeting systems are incremental in nature and tend to focus on cost centers. Activity based budgeting (ABB) links strategic planning to the overall performance...(Solved)

Traditional budgeting systems are incremental in nature and tend to focus on cost centers. Activity based budgeting (ABB) links strategic planning to the overall performance measurement aimed at continuous improvement.

Required:

i Explain the weakness of traditional incremental budgeting systems.

ii Describe the main feature of activity based budgeting system and comment on its advantages.

Date posted: May 6, 2021.

- “It is now fairly and widely accepted that conventional cost accounting, distorts

management's view of business through unrepresentative overhead allocation

and inappropriate product costing. This is because...(Solved)

“It is now fairly and widely accepted that conventional cost accounting, distorts

management's view of business through unrepresentative overhead allocation

and inappropriate product costing. This is because the traditional approach usually absorbs

overhead costs across products solely on the basis of the direct labour involved in their

manufacture. As direct labour cost expressed as a proportion of total manufacturing cost

continues to fall, this leads to more an more distortion and misrepresentation of the impact

of particular products on total overhead costs (from Financial Times)

Required:

Briefly discuss the above statement and state what approaches are being adopted by management accountants to overcome such criticism.

Date posted: May 6, 2021.

- Briefly explain three methods that can be used to analyze uncertainty in cost-volume-profit (C-V-P) analysis.(Solved)

Briefly explain three methods that can be used to analyze uncertainty in cost-volume-profit (C-V-P) analysis.

Date posted: May 5, 2021.

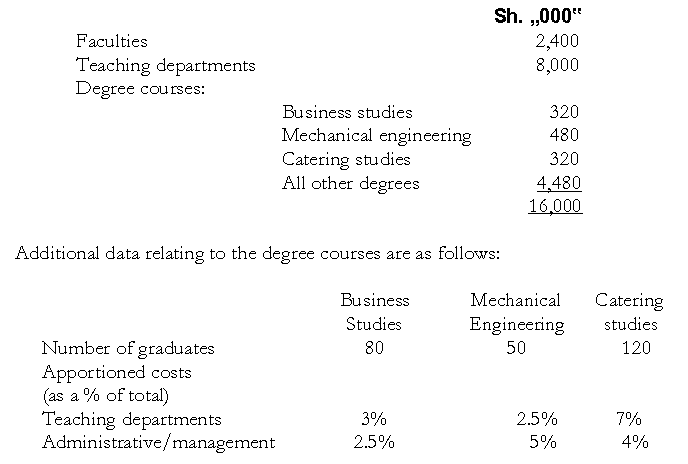

- A university offers a range of degree courses. The university's organization structure

consists of three faculties each with a number of teaching departments. In addition, there...(Solved)

A university offers a range of degree courses. The university's organization structure

consists of three faculties each with a number of teaching departments. In addition, there is

a university administrative/management function and a central services function.

The following cost information is available for the year ended 30 June 2002

a) Occupancy costs total Sh.15,000,000. Such costs are apportioned on the basis of area

used which is:

2. Administration/management costs:

Direct costs: Shs.17,750,000

Indirect costs: an apportionment of occupancy costs.

Direct and indirect costs are charged to degree courses on a percentage basis.

3. Faculty costs:

Direct costs: Shs. 7,000,000.

Indirect costs: an apportionment of occupancy and central services costs.

Direct and indirect costs are charged to teaching departments.

4. Teaching departments:

Direct costs: Shs. 55,250,000.

Indirect cost: an apportionment of occupancy costs and central services costs plus all

faculty costs.

Direct and indirect costs are charged to degree courses on a percentage basis.

5. Central services:

Direct costs: Sh.10,000,000

Indirect costs: an apportionment of occupancy costs.

6. Direct and indirect costs of central services have in previous years been charged to users

on a percentage basis. A study has now been completed which has estimated what user

areas would have paid external suppliers for the same services on an individual basis. For

the year ended 30 June 2002, the apportionment of central services costs is to be

recalculated in a manner which recognizes the cost/savings achieved by using the central

services facilities instead of using external service companies. This is to be done by

apportioning the overall savings to user areas in proportion to their share of the

estimated external costs.

7. The estimated external cost of service provision are as follows:

2. Administration/management costs:

Direct costs: Shs.17,750,000

Indirect costs: an apportionment of occupancy costs.

Direct and indirect costs are charged to degree courses on a percentage basis.

3. Faculty costs:

Direct costs: Shs. 7,000,000.

Indirect costs: an apportionment of occupancy and central services costs.

Direct and indirect costs are charged to teaching departments.

4. Teaching departments:

Direct costs: Shs. 55,250,000.

Indirect cost: an apportionment of occupancy costs and central services costs plus all

faculty costs.

Direct and indirect costs are charged to degree courses on a percentage basis.

5. Central services:

Direct costs: Sh.10,000,000

Indirect costs: an apportionment of occupancy costs.

6. Direct and indirect costs of central services have in previous years been charged to users

on a percentage basis. A study has now been completed which has estimated what user

areas would have paid external suppliers for the same services on an individual basis. For

the year ended 30 June 2002, the apportionment of central services costs is to be

recalculated in a manner which recognizes the cost/savings achieved by using the central

services facilities instead of using external service companies. This is to be done by

apportioning the overall savings to user areas in proportion to their share of the

estimated external costs.

7. The estimated external cost of service provision are as follows:

Central services are apportioned as detailed in (5) above.

The total number of graduates from the university in the year to 30 June 2002 was 2,500.

Required:

a) Prepare a flow diagram which shows the apportionment of costs to user areas. (No value needs to be shown).

b) Calculate the average cost per graduate for the year ended 30 June 2002, for the

university and for each of the degree courses in business studies, mechanical engineering

and catering studies (round your values to the nearest Sh.1,000)

c) Suggests reasons for any differences in the average cost per graduate from one degree

course to another, and discuss briefly the relevance of such information to the

university's management.

Central services are apportioned as detailed in (5) above.

The total number of graduates from the university in the year to 30 June 2002 was 2,500.

Required:

a) Prepare a flow diagram which shows the apportionment of costs to user areas. (No value needs to be shown).

b) Calculate the average cost per graduate for the year ended 30 June 2002, for the

university and for each of the degree courses in business studies, mechanical engineering

and catering studies (round your values to the nearest Sh.1,000)

c) Suggests reasons for any differences in the average cost per graduate from one degree

course to another, and discuss briefly the relevance of such information to the

university's management.

Date posted: May 5, 2021.

- Large service organizations such as banks and hospitals used to be noted for their lack of

standard costing systems and their relatively unsophisticated budgeting and control...(Solved)

Large service organizations such as banks and hospitals used to be noted for their lack of

standard costing systems and their relatively unsophisticated budgeting and control systems

compared to the practice in large manufacturing organizations. But this is changing any

many large service organizations are now reversing their use of management accounting techniques.

Required:

a) Explain which features of large service organizations encourage the application of

activity-based approaches to the analysis of cost information.

b) Explain which features of service organizations may create problems for the application

of activity-based costing.

c) Explain the uses of activity-based cost information in service industries.

Date posted: May 5, 2021.

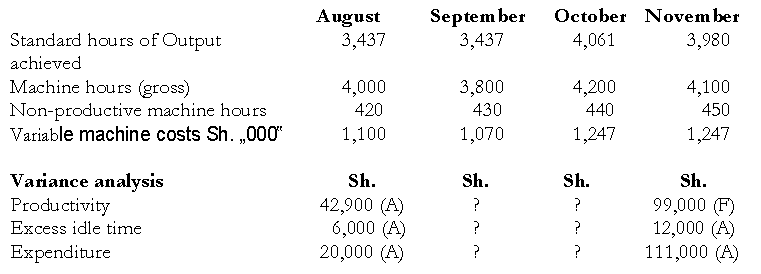

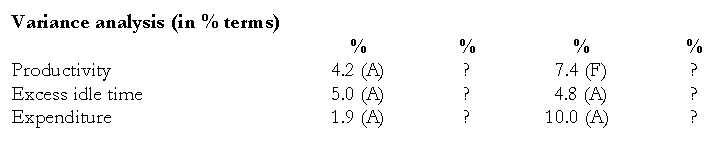

- Tritech Ltd. has semi-automatic machine process in which a number of tasks are performed.

A system of standard costing and budgetary control is in operation. The...(Solved)

Tritech Ltd. has semi-automatic machine process in which a number of tasks are performed.

A system of standard costing and budgetary control is in operation. The process is

controlled by machine attendants who are paid a fixed rate per hour of process time. The

process has recently been reorganized as part of an ongoing total quality management

programme in the company.

The nature of the process is such that the machines incur variable costs even during nonproductive

(idle time) hours. Non-productive hours include time spent on the rework of

products.

(Note: Gross machine hours = productive hours + non-productive hours)

The standard data for the machine process are as follows:

1. Standard non-productive (idle time) hours as a percentage of gross machine hour is

10%.

2. Standard variable machine cost per gross hour is Sh.270.

3. Standard output productivity is 100% that is one standard hour of work is expected in

each productive machine hour.

4. Machine costs are charged to production output at a rate per standard hour sufficient to

absorb the cost of the standard level of non-productive time.

Actual data for the period August to November 2002 have been summarized below:

Required:

a) Calculate the machine variances for productivity, excess idle time and expenditure for

each of the two months of September and October.

b) In order to highlight the trend of variances in the months from August to

November 2002, express each as a percentage term as follows:

i Productivity variance as a percentage of standard cost of production achieved.

ii Excess idle time variance as a percentage of expected idle time.

iii Expenditure variance as a percentage of hours paid for all standard machine cost.

c) Comment on the trend of variances in the August to November period and possible

inter-relationships. Particularly in the context of the total quality management

programme which is being implemented.

Required:

a) Calculate the machine variances for productivity, excess idle time and expenditure for

each of the two months of September and October.

b) In order to highlight the trend of variances in the months from August to

November 2002, express each as a percentage term as follows:

i Productivity variance as a percentage of standard cost of production achieved.

ii Excess idle time variance as a percentage of expected idle time.

iii Expenditure variance as a percentage of hours paid for all standard machine cost.

c) Comment on the trend of variances in the August to November period and possible

inter-relationships. Particularly in the context of the total quality management

programme which is being implemented.

Date posted: May 5, 2021.

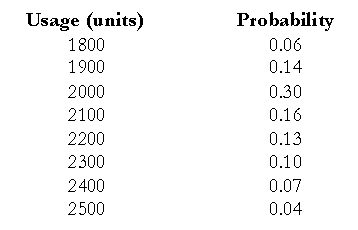

- A company has determined that the EOQ for its only raw material is 2000 units every 30

days. The company knows with certainty that a four-day...(Solved)

A company has determined that the EOQ for its only raw material is 2000 units every 30

days. The company knows with certainty that a four-day lead time is required for

ordering. The following is the probability distribution of estimated usage of the raw

material for the month of December 2002.

Stock-outs will cost the company Sh.100 per unit and the average monthly holding cost

will be Sh.10 per unit

Required

i Determine the optimal safety stock

ii Compute the probability of being out of stock.

Stock-outs will cost the company Sh.100 per unit and the average monthly holding cost

will be Sh.10 per unit

Required

i Determine the optimal safety stock

ii Compute the probability of being out of stock.

Date posted: May 4, 2021.