-

The following transactions relate to Jakayo Traders for the month of December 2010:

Determine:

(i) VAT payable by (or refundable to) Jakayo Traders for the month of December 2010.

(ii) Comment on any information not used in your computation under (i) above.

Determine:

(i) VAT payable by (or refundable to) Jakayo Traders for the month of December 2010.

(ii) Comment on any information not used in your computation under (i) above.

Date posted:

February 15, 2019

-

Discuss three challenges associated with the harmonization of taxation policies across regions and trading blocks

Date posted:

February 15, 2019

-

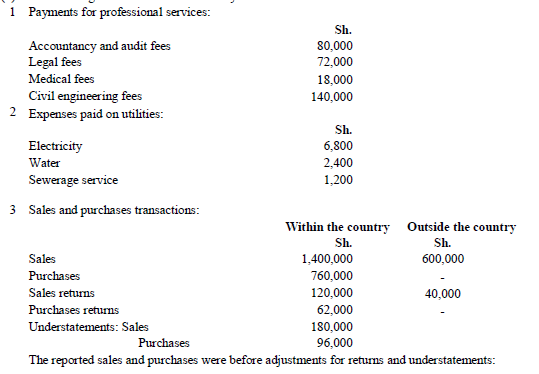

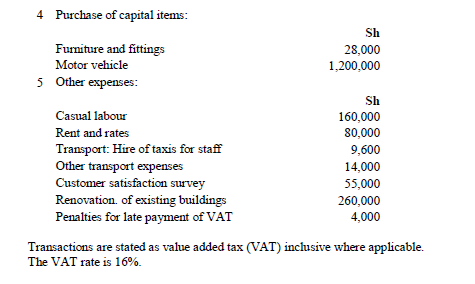

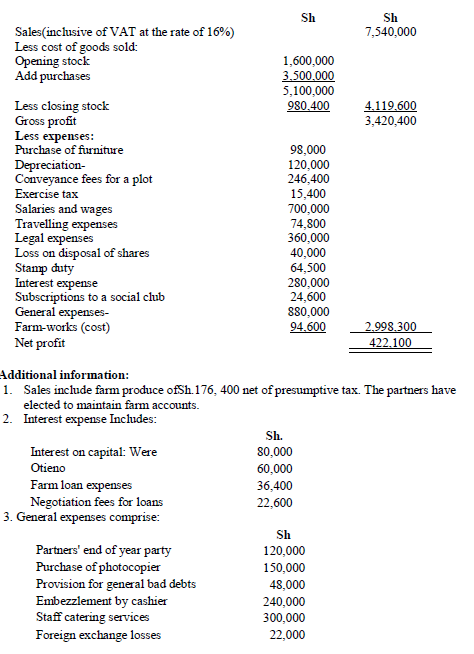

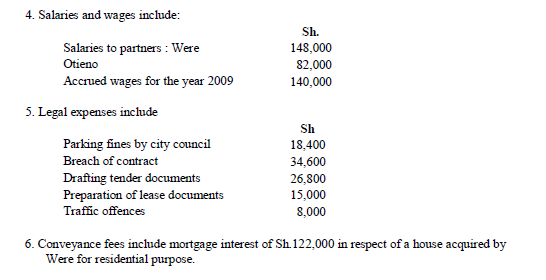

Were and Otieno are in partnership trading as Woti Enterprises. They share profits and losses in the ratio of 2:3 respectively. The partnership's statement of comprehensive income for the year ended 31 December 2010 is as shown below

Prepare:

(i) A statement of adjusted taxable profit or loss for the partnership business for the year ended 31 December 2010

(ii) A schedule showing total taxable income for each partner for the year ended 31 December 2010

Prepare:

(i) A statement of adjusted taxable profit or loss for the partnership business for the year ended 31 December 2010

(ii) A schedule showing total taxable income for each partner for the year ended 31 December 2010

Date posted:

February 15, 2019

-

With reference to the East African Community Customs Management Act or other relevant legislation applicable in your country, highlight four functions of the directorate of customs

Date posted:

February 15, 2019

-

Briefly explain four circumstances under which a taxpayer might be exempted from paying installment tax.

Date posted:

February 15, 2019

-

Outline four categories of goods which are subject to customs control under the Customs and excise Act.

Date posted:

February 15, 2019

-

Identify four documents required in support of an application for refund of value added tax (VAT) paid in respect of bad debts

Date posted:

February 15, 2019

-

Highlight five circumstances under which customs duty paid might be refunded

Date posted:

February 15, 2019

-

Outline six contents of a notice of assessment.

Date posted:

February 15, 2019

-

Beta Supermarket Ltd. is registered for VAT. During the month of January 2013, the supermarket had the following transactions

January

1 Sold goods on credit to Mwamba Enterprises for Sh. 400,000.

2 Purchased goods on credit from Hekima Traders for Sh. 200,000

2 Paid for catering expenses Sh. 68,000 by cash

3 Mwamba Enterprises returned goods valued at Sh.60, 000, and received a credit note.

4 Exported goods to Uzalendo Ltd., a company based in Rwanda for Sh. 300,000

5 Purchased stationery for Sh. 84,000 on credit from Smart Books Bookshop.

9 Purchased goods for Shs 800,000 from Uchumi Enterprises on credit

12 Imported goods from Canada for Sh. 900,000 exclusive of import duty of 25% and value added tax at 16%.

16 Received a debit note of Sh. 48,000 from Uchumi Enterprises

17 Paid electricity bills amounting to Sh. 24,000 by cheque

20 Engaged an auditor and paid him Sh. 60,000 for auditing the supermarket‘s inventory.

21 Sold goods worth Sh. l,400,000 to the Ministry of Youth and Sports

24 Bought spare .parts for repair of motor vehicles for Sh. 120,000

25 Sold goods on credit to Jawabu Enterprises for Sh. 800,000

30 Made cash sales of Sh. 200,000 and banked the cash on the same day

The above transactions are stated inclusive of VAT at the rate of 16% where applicable and unless otherwise stated

Determine A value added tax (VAT) account for the month of January 2013

Date posted:

February 15, 2019

-

Outline four offences under the value added tax (VAT) Act

Date posted:

February 15, 2019

-

The VAT Act requires a registered person to notify the commissioner' within 14 days of changes in certain particulars of a business.

Suggest six such changes whose details need to be notified to the commissioner

Date posted:

February 15, 2019

-

Evaluate four measures under Customs and Excise Act that are designed to prevent dumping in your country

Date posted:

February 15, 2019

-

Explain three benefits that could be derived from changing zero rated supplies to exempt supplies in your country

Date posted:

February 15, 2019

-

Outline four ways through which a government could prevent loss of revenue from imports

Date posted:

February 15, 2019

-

The revenue authority of your country has recently launched an online based integrated tax management system whose aim is to make it more convenient for firms and individuals to pay tax.

In light of this statement:

(i) Briefly explain how an online based integrated tax management system works.

(ii) List three types of tax returns that are filed under the system.

(iii) Evaluate five benefits that are derived from use of the system over the traditional model of filing tax returns

Date posted:

February 15, 2019

-

Highlight four circumstances under which the government might revoke the licence of a manufacturer of excisable goods.

Date posted:

February 15, 2019

-

Argue four cases in favor of introduction of capital gains tax (CGT) in most countries

Date posted:

February 15, 2019

-

Outline four requirements for a valid memorandum of appeal

Date posted:

February 15, 2019

-

Summarize four details that are required to accompany the list submitted to the revenue authority on employees who have received lump sum payment from the employer.

Date posted:

February 15, 2019

-

Explain the following terms in the 'context of customs and excise duty:

(i) Prohibited goods.

(ii) Restricted goods

Date posted:

February 15, 2019

-

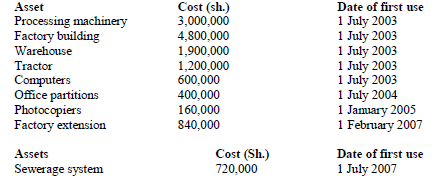

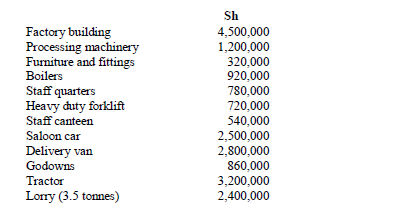

Ujenzi Limited maintained the following assets in its fixed registers as at 31 December 2007

Determine Capital allowances due to Ujenzi limited for the year ended 31 December 2007

Determine Capital allowances due to Ujenzi limited for the year ended 31 December 2007

Date posted:

February 14, 2019

-

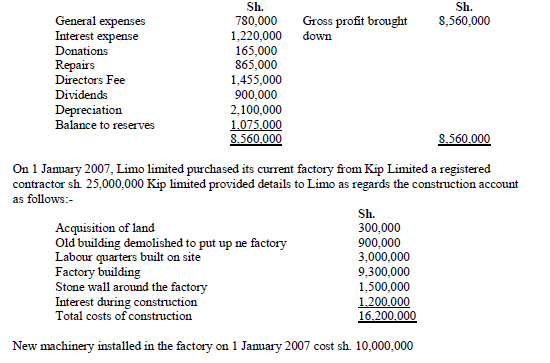

Limo Limited prepares its accounts to 31 December each year. The company‘s trading profit and loss account for the year ended 31 December 2007 is presented below

Determine:

i) Capital allowances due to Limo Limited for the year ended 31 December 2007

ii) Taxable profit (or loss) of Limo Limited for the year ended 31 December 2007

iii) Tax liability (if any) from the profit (or loss) computed in (ii) above

Determine:

i) Capital allowances due to Limo Limited for the year ended 31 December 2007

ii) Taxable profit (or loss) of Limo Limited for the year ended 31 December 2007

iii) Tax liability (if any) from the profit (or loss) computed in (ii) above

Date posted:

February 14, 2019

-

Citing two reasons, argue the case against capital allowances in an economy

Date posted:

February 14, 2019

-

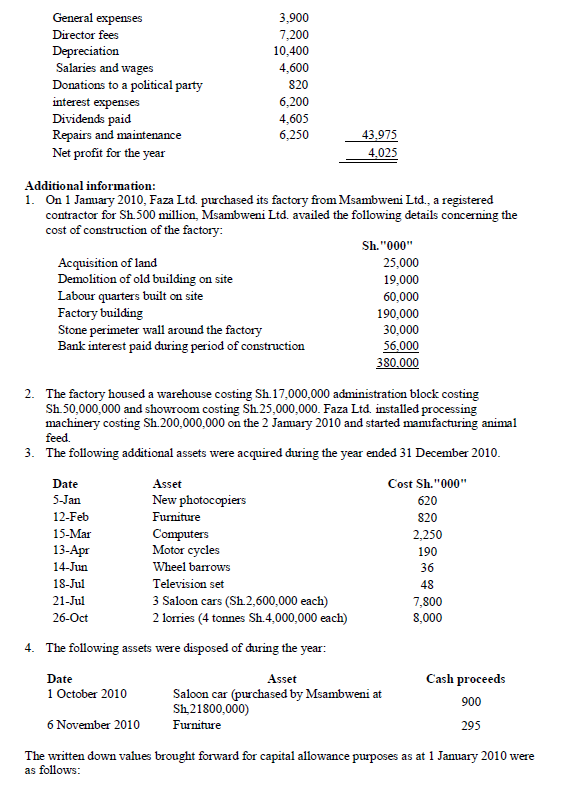

Faza Ltd. a large scale manufacturing company, has provided you with the following information for the year ended 31December 2010

Compute for Faza Ltd. for the year ended 31 December 2010:

(i) Capital allowances.

(ii) Taxable profit

Compute for Faza Ltd. for the year ended 31 December 2010:

(i) Capital allowances.

(ii) Taxable profit

Date posted:

February 14, 2019

-

Heshima Ltd. commenced operations on 1 January 2011 after incurring the following expenditure

Compute for Heshima Ltd. for the year ended 31 ended 2011

i) Capital allowances

ii) Adjusted taxable profit

Compute for Heshima Ltd. for the year ended 31 ended 2011

i) Capital allowances

ii) Adjusted taxable profit

Date posted:

February 14, 2019

-

Turbo Mining Company Ltd started prospecting for minerals in Turkana in year 2008. Expenditure relating to research, testing and winning access to minerals amounted to Sh.48 million.

The company paid Sh. 124 million to the government to acquire the rights over the minerals and shs.180 million for purchase of land.

The following assets were constructed or purchased during the year 2009:

1. Labour quarters were constructed at a cost of Sh. 15 million.

2. Senior manager's house was constructed on the site at a cost of Sh.6 million.

3. The director's house was acquired at a nearby trading centre at a cost of Sh.9 million.

4. Specialised processing machineries for mining were acquired at a cost of Sh.860 million.

5. Computers were purchased at a cost of Sh.0.72 million.

6. A forklift was acquired at a cost of Sh.4.5 million.

7. A saloon car for the general manager was purchased at a cost of Sh.3 million.

8. Office furniture was acquired at a cost of Sh. 1.5 million.

9. An aircraft was acquired for Sh. 144 million.

10. A store was constructed at a cost of Sh.21 million.

Determine The capital allowances due to the company for the years ended 31 December 2009, 2010 and 2011.

Date posted:

February 14, 2019

-

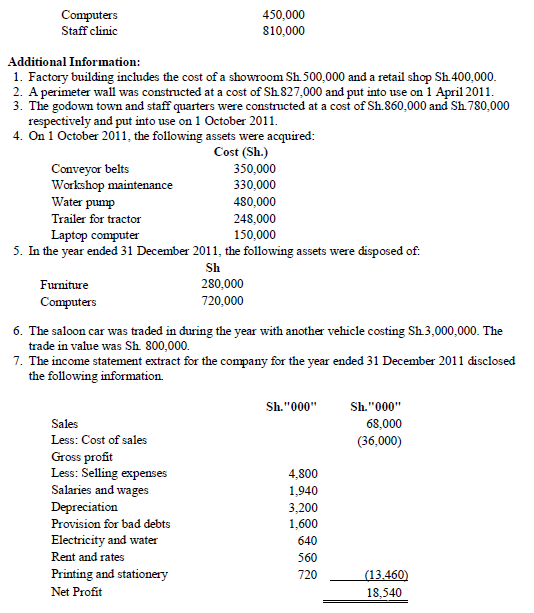

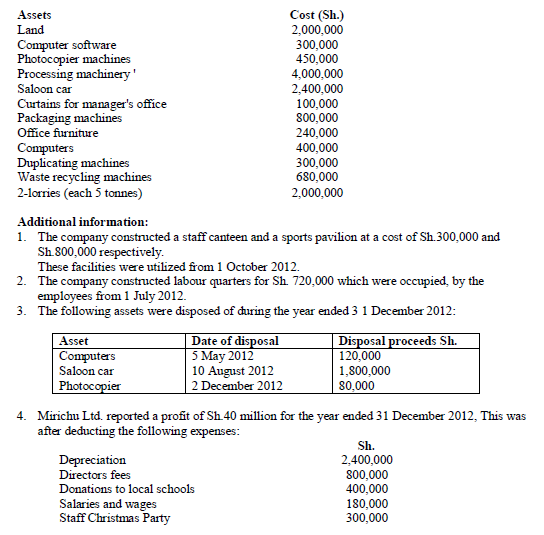

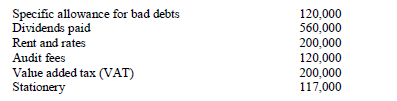

Mirichu Ltd. processes milk for sale in the local market.The company started its operations on 1 January 2012 after constructing two factory building at a cost of Sh.9 million each. Other assets acquired by the company on commencement of its operations included

Determine:

a) The capital allowances due to Mirichu Ltd. for the year ended 31 December 2012.

b) The taxable profit or loss for Mirichu Ltd. for the year ended 31 December 2012.

c) The tax- payable, if any, for the year ended 31 December 2012.

Determine:

a) The capital allowances due to Mirichu Ltd. for the year ended 31 December 2012.

b) The taxable profit or loss for Mirichu Ltd. for the year ended 31 December 2012.

c) The tax- payable, if any, for the year ended 31 December 2012.

Date posted:

February 14, 2019

-

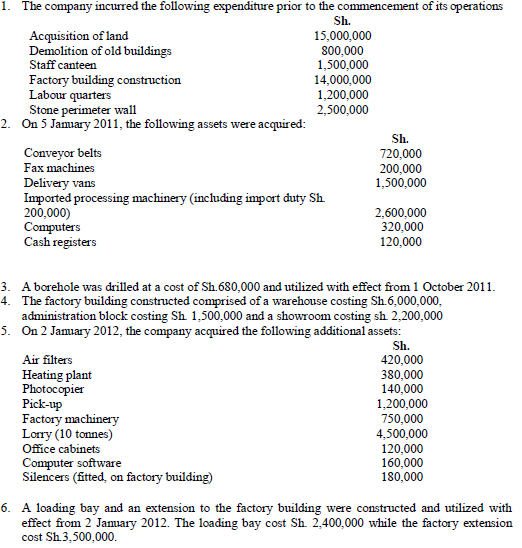

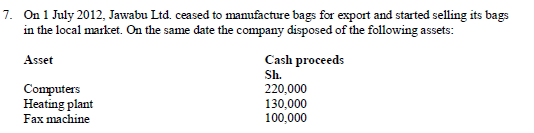

Jawabu Ltd. commenced its operations on 1 January 2011 after obtaining a licence to manufacture leather bags for export.

The following information relates to the company's operations for the financial years ended 31 December 2011 and 2012:

Determine Capital allowances due to Jawabu Ltd. for each of the two years ended 31 December 2011 and 2012.

Determine Capital allowances due to Jawabu Ltd. for each of the two years ended 31 December 2011 and 2012.

Date posted:

February 14, 2019

-

Poland Mining Company Ltd. started prospecting for titanium in Mombasa in year 2011. Expenditure relating to research, testing and winning access to titanium amounted to Sh.240 million. The company paid Sh.720 million to the government to acquire rights over the titanium and Sh.210 million for the purchase of land.

The following assets were constructed or purchased during the year 2012:

1. Two graders were purchased at a total cost of Sh.16, 000,000.

2. A forklift was acquired at a cost of Sh.6, 000,000.

3. A store was constructed at a cost of Sh.36, 000,000

4. Office furniture was acquired at a cost of Sh.2, 400,000.

5. Labor quarters were constructed at a cost of Sh.42, 000,000.

6. Ten Lorries (5 tonnes each) were acquired at a total cost of Sh.30, 000,000.

7. Specialized processing machines for mining were acquired at a cost of Sh.960, 000,000.

8. A staff clinic was constructed at a cost of Sh.12, 000,000 .

9. Computers were purchased at a cost of Sh.480, 000.

10. A ship (600 tonnes) was acquired at a cost of Sh.450, 000,000.

11. Three saloon cars for official use were acquired at a total cost of Sh.9, 000,000.

Determine Capital allowances due to Poland Mining Company Ltd. for the two years ended 31 December 2012 and 31 December 2013

Date posted:

February 14, 2019