-

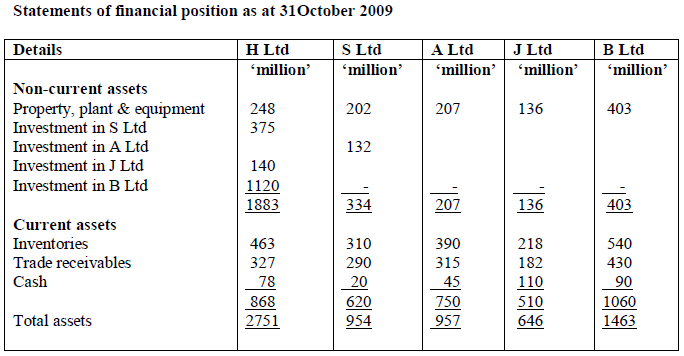

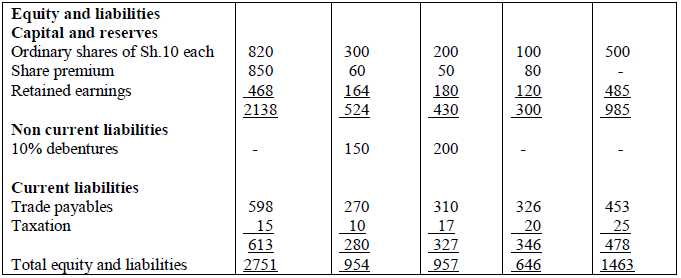

The statements of financial position of H Ltd, S Ltd, A Ltd, J Ltd and B Ltd as at 31 October 2009 are as follows:

Additional information:

1. H Ltd purchased 75% of the ordinary shares of S Ltd on 1 November 2007, when the balance of the earnings of S Ltd was sh. 80 million.

2. S Ltd purchased 30% of the ordinary shares of A Ltd on 1 November 2007 were sh. 140 million.

3. H Ltd and another company, Ukwala Ltd, each bought 50% of the share capital of J Ltd on 1 May 2009. H Ltd and Ukwala Ltd have a joint control of J Ltd. Both companies are to account for their Joint venture using proportionate consolidation; combining items on a line by line basis. J Ltd’s retained earnings on 1 May 2009 were sh. 110 million.

4. On 1 May 2009, H Ltd acquired 45 million ordinary shares of shs. 10 each in B Ltd when the retained earnings of B Ltd were sh.400 million.

5. On 1 May 2009, the fair values of the identifiable net assets of B Ltd, approximated book value except for leasehold whose book value was sh. 40 million below its fair value. The property is depreciated to nil residual value over the term of the lease. On 1 May 2009, there were 10 years remaining of the lease.

6. On 1 November 2007, the book value of the identifiable net assets of A Ltd was sh. 20 million below their fair value. The assets revalued are not to be depreciated.

7. Included in the closing inventory of H Ltd is shs. 12 million worth of goods purchased from J Ltd which cost sh. 8 million.

8. In the year ended 31 October 2009, H Ltd sold goods to B Ltd at a price of sh. 15 million. H Ltd had marked up these goods by 50% on cost. B Ltd held 50% of these goods in its closing inventory on 31 October 2009.

9. As at 31 October 2009, H Ltd owed J Ltd sh. 12 million. As at the same date, S Ltd owed H Ltd sh. 13 million and A Ltd Sh 20 million. All the current accounts between the companies were in agreement.

10. As at 31 October 2009, it was estimated that since the date of acquisition, goodwill had suffered impairment loss by the following percentages:

S Ltd = 40%

B Ltd = 25%

The goodwill of J Ltd and the premium on acquisition of A Ltd had not been impaired since the date of acquisition.

11. It is groups’ policy to value the non-controlling interest at fair value or the market value. The fair value of the non-controlling interest in S Ltd at the date of acquisition was Sh. 120 million, while the fair value of the non-controlling interest in B Ltd, at the date of acquisition was shs. 124 million.

Required:

Consolidated statement of financial position as at 31 October 2009, J Ltd should be accounted for using the proportionate consolidation method as per IAS 31(Interest in Joint ventures)

Additional information:

1. H Ltd purchased 75% of the ordinary shares of S Ltd on 1 November 2007, when the balance of the earnings of S Ltd was sh. 80 million.

2. S Ltd purchased 30% of the ordinary shares of A Ltd on 1 November 2007 were sh. 140 million.

3. H Ltd and another company, Ukwala Ltd, each bought 50% of the share capital of J Ltd on 1 May 2009. H Ltd and Ukwala Ltd have a joint control of J Ltd. Both companies are to account for their Joint venture using proportionate consolidation; combining items on a line by line basis. J Ltd’s retained earnings on 1 May 2009 were sh. 110 million.

4. On 1 May 2009, H Ltd acquired 45 million ordinary shares of shs. 10 each in B Ltd when the retained earnings of B Ltd were sh.400 million.

5. On 1 May 2009, the fair values of the identifiable net assets of B Ltd, approximated book value except for leasehold whose book value was sh. 40 million below its fair value. The property is depreciated to nil residual value over the term of the lease. On 1 May 2009, there were 10 years remaining of the lease.

6. On 1 November 2007, the book value of the identifiable net assets of A Ltd was sh. 20 million below their fair value. The assets revalued are not to be depreciated.

7. Included in the closing inventory of H Ltd is shs. 12 million worth of goods purchased from J Ltd which cost sh. 8 million.

8. In the year ended 31 October 2009, H Ltd sold goods to B Ltd at a price of sh. 15 million. H Ltd had marked up these goods by 50% on cost. B Ltd held 50% of these goods in its closing inventory on 31 October 2009.

9. As at 31 October 2009, H Ltd owed J Ltd sh. 12 million. As at the same date, S Ltd owed H Ltd sh. 13 million and A Ltd Sh 20 million. All the current accounts between the companies were in agreement.

10. As at 31 October 2009, it was estimated that since the date of acquisition, goodwill had suffered impairment loss by the following percentages:

S Ltd = 40%

B Ltd = 25%

The goodwill of J Ltd and the premium on acquisition of A Ltd had not been impaired since the date of acquisition.

11. It is groups’ policy to value the non-controlling interest at fair value or the market value. The fair value of the non-controlling interest in S Ltd at the date of acquisition was Sh. 120 million, while the fair value of the non-controlling interest in B Ltd, at the date of acquisition was shs. 124 million.

Required:

Consolidated statement of financial position as at 31 October 2009, J Ltd should be accounted for using the proportionate consolidation method as per IAS 31(Interest in Joint ventures)

Date posted:

December 10, 2021

-

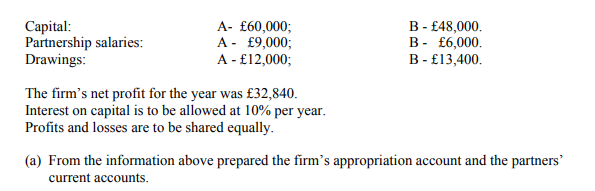

Draw up a profit and loss appropriation account for the year ended 31 December 2007

i. Net profits sh30,350

ii. Interest to be charged on capitals: W sh2,000; Psh1,500; H sh900

iii. Interest to be charged on drawings; W sh240; P sh180; H sh130

iv. Salaries to be credited: P sh2,000; H sh3,500.

v. Profits to be shared: W 50%; P 30%; H20%.

vi. Current accounts: balances b/f W sh1,860; P sh946; H sh717

vii. Capital accounts: balances b/f W sh40,000; P sh30,000; H sh18,000

viii. Drawings: W sh9,200; P sh7,100; H sh6,900.

Date posted:

December 10, 2021

-

Read the following and answer the questions below.

A and B own a grocery shop. Their first financial year ended on 31 December 2002.

The following balances were taken from the books on that date:

Date posted:

December 10, 2021

-

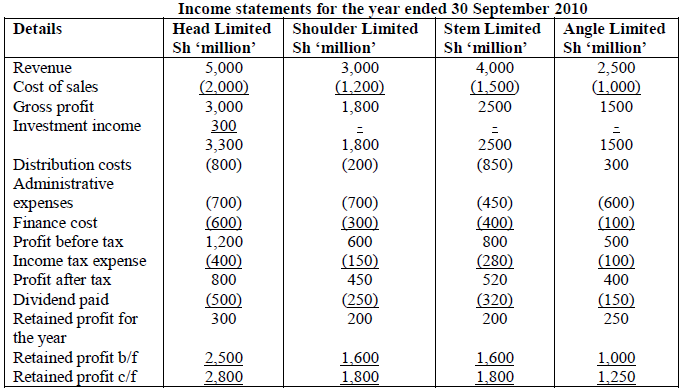

Head Limited sold off its entire shareholding of 80% in Shoulder Limited and acquired 75% of the shares of Stem Limited during the year ended 30 September 2010. Head Limited also acquired 40% of the shares of Angle Limited.

The following income statements relate to the four companies:

Additional information:

1. Head Limited had acquired it s shareholding in Shoulder Limited at a cost of Sh 2200 million on 1 October 2007 when the retained earnings of Shoulder Limited were Sh.500 million. The ordinary share capital of Shoulder Limited was Sh. 2,000 million and there were no other reserves. The fair value of the non-controlling interest in Shoulder Limited on the same date was Sh.550 million.

2. During the year ended 30 September 2010, Head Limited acquired the investment in Stem Limited and Angle Limited. The details of the acquisitions are as follows:

Additional information:

1. Head Limited had acquired it s shareholding in Shoulder Limited at a cost of Sh 2200 million on 1 October 2007 when the retained earnings of Shoulder Limited were Sh.500 million. The ordinary share capital of Shoulder Limited was Sh. 2,000 million and there were no other reserves. The fair value of the non-controlling interest in Shoulder Limited on the same date was Sh.550 million.

2. During the year ended 30 September 2010, Head Limited acquired the investment in Stem Limited and Angle Limited. The details of the acquisitions are as follows:

On the date of its acquisition, Stem Limited had an item of plant that was Sh.270 million below its fair value. Plant is depreciated at 20% per annum with a full year’s charge in the year of purchase or revaluation.

3. On 1 July 2010, Head Limited sold its investment in Shoulder Limited at a price of Sh.3,430 million. This disposal has not been reflected in the income statement of Head Limited.

4. During the year, the companies traded as follows:

On the date of its acquisition, Stem Limited had an item of plant that was Sh.270 million below its fair value. Plant is depreciated at 20% per annum with a full year’s charge in the year of purchase or revaluation.

3. On 1 July 2010, Head Limited sold its investment in Shoulder Limited at a price of Sh.3,430 million. This disposal has not been reflected in the income statement of Head Limited.

4. During the year, the companies traded as follows:

5. Goodwill of Shoulder Limited had been impaired by half as at 1 October 2009. Any goodwill arising in Stem Limited and Angle Limited is impaired by 20%.

6. All dividends were paid on 31 August 2010.

Required:

a) The group income statement for the year ended 30 September 2010.

b) The statement of changes in equity showing only the retained profits column.

5. Goodwill of Shoulder Limited had been impaired by half as at 1 October 2009. Any goodwill arising in Stem Limited and Angle Limited is impaired by 20%.

6. All dividends were paid on 31 August 2010.

Required:

a) The group income statement for the year ended 30 September 2010.

b) The statement of changes in equity showing only the retained profits column.

Date posted:

December 10, 2021

-

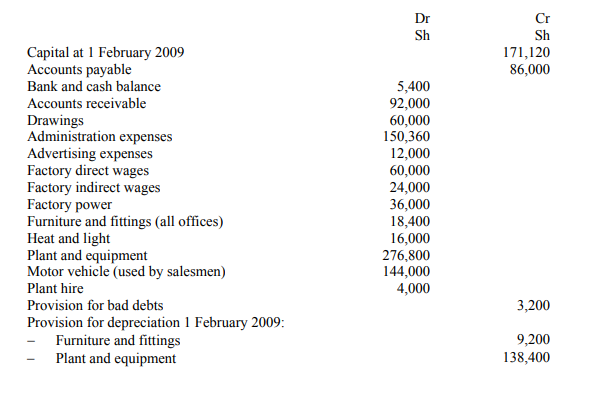

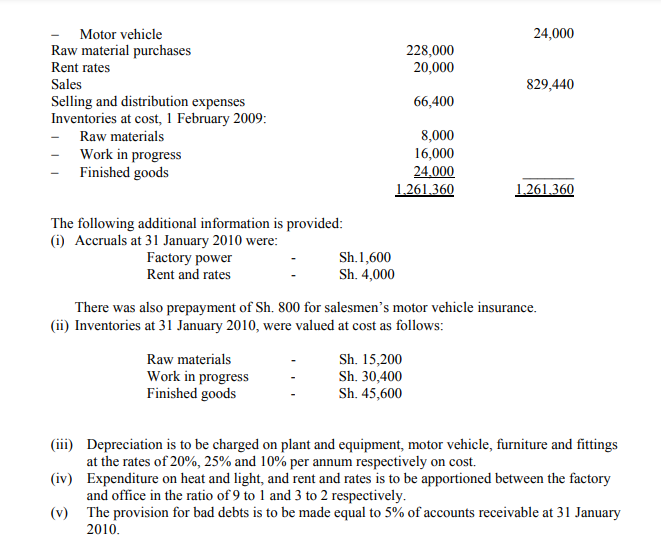

Bibi Maridadi owns and manages a small manufacturing business. The following balances have

been extracted from her books of account at 31 January 2009:

Required:

Using the vertical method, prepare Bibi Maridadi’s manufacturing, trading and profit and loss

account for the year ended 31 January 1986 and a balance sheet as at that date.

Required:

Using the vertical method, prepare Bibi Maridadi’s manufacturing, trading and profit and loss

account for the year ended 31 January 1986 and a balance sheet as at that date.

Date posted:

December 10, 2021

-

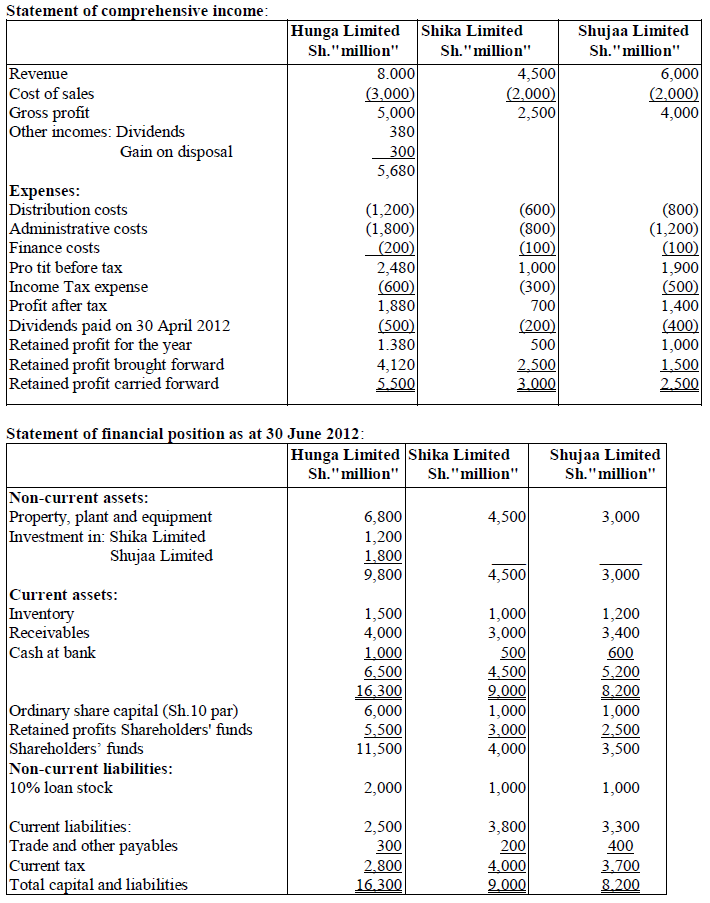

Hunga Limited, a company quoted on the securities exchange, acquired 80% of Shika Limited several years ago. On 1 January 2012 Hunga limited sold half of its investment in Shika Limited and acquired 75% of the equity shares of Shujaa Limited.

The financial statements for the year ended 30 June 2012 for the three companies are as given below.

Additional information:

1. Hunga Limited had acquired its shareholding in Shika Limited for Sh.2,400 million when the retained profits of Shika Limited amounted to Sh. 1,500 million. There was no fair value adjustment at the time of this acquisition.

2. Hunga Limited sold half of the investment in Shika Limited for Sh.1.500 million. This disposal has already been accounted for by Hunga Limited but not by the group. The fair value of the remaining investment in Shika Limited was Sh.1, 300 million on the date of disposal.

3. Between 1 January 2012 and 30 June 2012. Hunga Limited sold to Shujaa Limited goods worth Sh.500 million reporting, a profit of Sh. 100 million. Half of the goods were still in the inventory of Shujaa Limited as at 30 June 2012.

4. Intercompany receivables and payables were as follows as at 30 June 2012:

Additional information:

1. Hunga Limited had acquired its shareholding in Shika Limited for Sh.2,400 million when the retained profits of Shika Limited amounted to Sh. 1,500 million. There was no fair value adjustment at the time of this acquisition.

2. Hunga Limited sold half of the investment in Shika Limited for Sh.1.500 million. This disposal has already been accounted for by Hunga Limited but not by the group. The fair value of the remaining investment in Shika Limited was Sh.1, 300 million on the date of disposal.

3. Between 1 January 2012 and 30 June 2012. Hunga Limited sold to Shujaa Limited goods worth Sh.500 million reporting, a profit of Sh. 100 million. Half of the goods were still in the inventory of Shujaa Limited as at 30 June 2012.

4. Intercompany receivables and payables were as follows as at 30 June 2012:

5. As at 1 July 2011, half of the goodwill of Shika Limited had been impaired. The goodwills of the companies were not impaired in the current year to 30 June 2012. The group uses the partial goodwill method when preparing the consolidated financial statements.

Required;-

a) Group statement of comprehensive income for the year ended 30 June 2012.

b) Group statement of financial position as at 30 June 2012.

5. As at 1 July 2011, half of the goodwill of Shika Limited had been impaired. The goodwills of the companies were not impaired in the current year to 30 June 2012. The group uses the partial goodwill method when preparing the consolidated financial statements.

Required;-

a) Group statement of comprehensive income for the year ended 30 June 2012.

b) Group statement of financial position as at 30 June 2012.

Date posted:

December 10, 2021

-

List some of the the quasi-government institutions that are stakeholders in tourism development and state their roles

Date posted:

December 10, 2021

-

Describe the phases of tourism policy formulation

Date posted:

December 10, 2021

-

Describe The Tributary Economic System in Buganda Kingdom

Date posted:

December 8, 2021

-

Explain the three forms of feudal rent that existed in the feudal economic society

Date posted:

December 8, 2021

-

Describe The Slave Mode of Production in 19th Century in Africa

Date posted:

December 8, 2021

-

Special types of prison in Kenya

Date posted:

December 7, 2021

-

Jadili Ngoma za Waswahili

Date posted:

December 6, 2021

-

Eleza dini ya Waswahili

Date posted:

December 6, 2021

-

Elezea kazi mbalimbali zilizofanywa na Waswahili

Date posted:

December 6, 2021

-

Ni vipi Kiswahili kinaweza kuimarisha umoja katika Afrika Mashariki na kati?

Date posted:

December 6, 2021

-

"Kiswahili sio lugha ya Afrika Mashariki tu,bali ni lugha ya kimataifa."Jadili kauli hii

Date posted:

December 6, 2021

-

Huku ukitoa mifano jadili matatizo yanayokumba uundaji wa istilahi za kiswahili na jinsi yanavyoweza kutatuliwa

Date posted:

December 6, 2021

-

Kwa kutoa mifano, fafanua mbinu mbalimbali zinazotumiwa kuundia msamiati na istilahi za Kiswahili

Date posted:

December 6, 2021

-

Juhudi za kuendeleza kiswahili nchini Uganda baada ya uhuru bado hazijafaulu" jadili kauli hii

Date posted:

December 6, 2021

-

Eleza ni vipi sheng' inavyoathiri maendeleo ya kiswahili nchini Kenya na hatua zinazoweza kuchukuliwa ili kukabili

Date posted:

December 6, 2021

-

Tathmini mchango wa tume ya Mackey (1981) na time ya Koech (1999) katika kustawisha Kiswahili nchini Kenya

Date posted:

December 6, 2021

-

Eleza jinsi sera ya lugha nchini Tanzania ilivyosaidia lugha ya Kiswahili kupiga hatua kubwa katika matumizi nchini humo kuliko nchini Kenya baada ya uhuru

Date posted:

December 6, 2021

-

Taja vituo mbalimbali vya redio nchini Kenya ambavyo hutangaza kwa Kiswahili kisha ueleze ni vipi lugha hii inaendelezwa katika vituo hivyo

Date posted:

December 6, 2021

-

Tathmini kiwango cha matumizi ya lugha ya Kiswahili katika vituo vya redio na magazeti ya Tanzania

Date posted:

December 6, 2021

-

Kiswahili kinahitaji kusanifisha upya.Jadili kauli hii

Date posted:

December 6, 2021

-

Tathmini mchango wa kamati ya Kiswahili ya Afrika Mashariki(K.K.A.M) katika kusanifisha lugha ya Kiswahil

Date posted:

December 6, 2021

-

Eleza ni kwa nini lugha ya Kiswahili ilisanifishwa wakati wa ukoloni

Date posted:

December 6, 2021

-

Eleza ni kwa nini lahaja ya kiunguja ilichaguliwa kwa msingi wa kusanifisha lugha ya kiswahili na wala sio kimvita au kiamu

Date posted:

December 6, 2021

-

Huku ukitoa mfano mwafaka bainisha tofauti za kifonolojia na kimofolojia katika lahaja za kimvita ,kivumba na kiswahili sanifu

Date posted:

December 6, 2021